Lietuvių

Lietuvių Русский

Русский Қазақша

Қазақша Eesti

EestiFOMC Meeting Summary: June 2026

Fed Holds Rates as Warsh Debuts with Hawkish Tone

The fourth FOMC meeting of the year took place, at which the rate was (as expected) kept within the current range of 3.50–3.75%. The Fed reaffirmed its policy of maintaining ample reserves in the banking system.

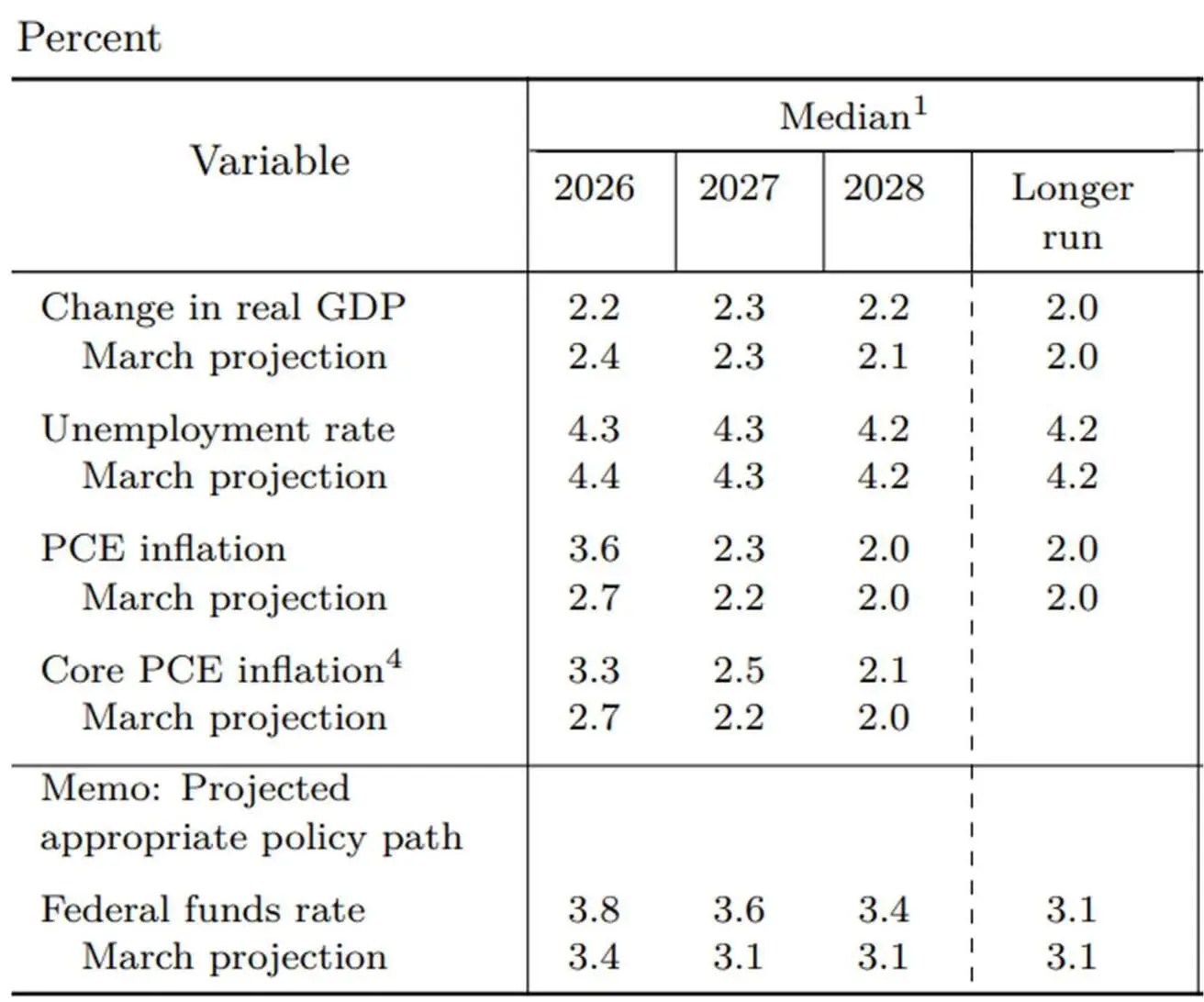

The Committee lowered its GDP forecast for 2026 to 2.2% and raised its inflation expectations to 3.6% for the PCE index and 3.3% Core PCE (personal consumption expenditures).

The median forecast for the federal funds rate was also raised: 3.8% by the end of 2026, which corresponds to a range of 3.75–4.00%, followed by cuts in 2027 and 2028.

Kevin Warsh's first press conference as Fed Chair began with the announcement of the creation of five working groups covering key areas of the regulator's work: Fed communications, the balance sheet, data sources, productivity and employment in the era of technological transformation, as well as the inflation framework. In essence, Warsh is opening a “new chapter” for the Fed with the intention of rethinking the very architecture of decision-making.

A separate emphasis was placed on data quality. Warsh stressed that the Fed should rely less on “echoes of the past” — that is, on outdated and lagging data — and orient itself more toward timely, current, and practically applicable information about the state of the economy. In this context, he noted the need to combine the best practices of the private sector and new tools made possible by AI into a single system that will allow the Fed to obtain higher-quality information in real time.

The second important point — Warsh signaled a departure from the customary forward guidance accompanying policy at press conferences.

Answering questions about the future path of the rate, the dot plots, and the format of communication, he declined to give direct guidance and emphasized several times that separate working groups would be addressing each of these areas.

Moreover, Warsh noted that financial markets should react first and foremost to incoming economic data, rather than to expectations of how the Fed will interpret that data. By his logic, the more markets independently assess the state of the real economy, separating strong data from weak and evaluating likely scenarios and tail risks, the more effectively the price mechanism works.

At the same time, this is not about abandoning the publication of the SEP — the summary of economic projections of FOMC participants — which will continue to be released. However, Warsh allowed that a new communication structure may emerge by the end of the year, and the format of the SEP itself may be revised.

Despite the fact that Warsh avoided direct forecasts in many of his answers, a few important points can still be drawn from his remarks. At the end of the press conference, he clarified his assessment of the labor market: to summarize the Committee's position, the labor market looks stable, and employment data are moving in a good direction. In other words, the labor market does not yet look like a factor that requires immediate policy easing.

As for the rate, here, Warsh, by contrast, emphasized the high degree of uncertainty. In his words, in the SEP, some members of the Committee believed that, given current events, the rate should remain at its current level or lower by the end of the year, while others saw it higher. Warsh himself, being the 19th participant in the discussion, did not submit his own forecast in the SEP.

This shows that within the Fed, there is no unified view on the further path of the rate, and the direction of policy remains open and will depend on new data.

Overall, Warsh's rhetoric looked more institutionally hawkish regarding the inflation target and the independence of the Fed, yet it need not necessarily be interpreted as a signal of immediate policy tightening. Rather, it can be read as an attempt to solve two problems at once: to show that the new chair, despite his association with the Trump administration, is not a “chair for cutting rates at any cost,” and to reassure markets on inflation risk by making clear that the Fed will not allow high inflation to take hold even under political pressure.

Ultimately, Kevin Warsh's first appearance can be described as an attempt to simultaneously reboot the Fed's communication architecture, confirm the regulator's independence, and cement confidence in its readiness to fight inflation, without setting a rigid path for further rate decisions in advance for the markets.

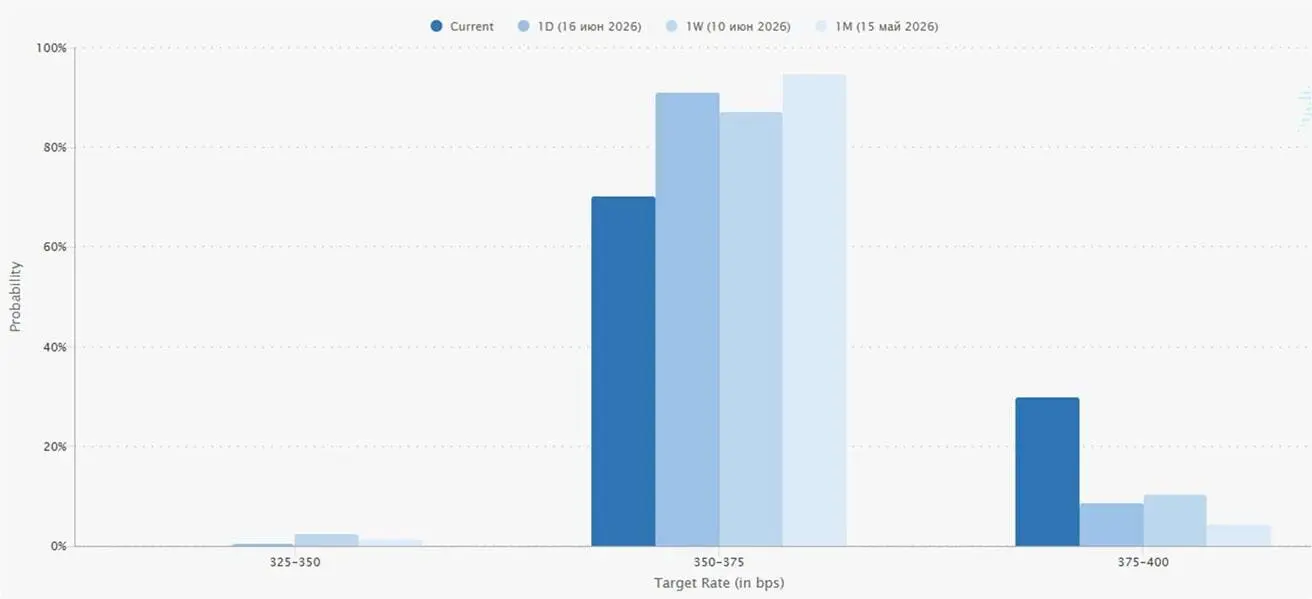

Market expectations for the Fed's rate still point to keeping the rate at its current level as the base-case scenario for the next meeting on July 29, but the probability of a hike has increased:

The markets' reaction at the session close was moderately defensive: equities and cryptocurrencies fell, the dollar strengthened, volatility rose, while long-dated Treasuries were almost unchanged:

-

S&P500 futures: −1.27%;

-

VIX: +9.80% (to 18.43);

-

Gold futures: −2.78%;

-

Dollar index futures: +0.83%;

-

TLT ETF on long-term U.S. Treasuries: −0.05%;

-

BTC/USD: −2.75%.

Why It Matters to Follow FOMC Meetings

The Federal Reserve's decisions directly affect the cost of capital worldwide. Equity and bond valuations, the U.S. dollar exchange rate, investment returns, and risk appetite all depend on them. Even when the rate is left unchanged, the Fed's rhetoric can set the tone for markets for a long time, signaling the prospect of tight policy, a pause, or future easing.