Lietuvių

Lietuvių Русский

Русский Қазақша

Қазақша Eesti

EestiJune 22 – 28, 2026: Weekly economic update

Key market updates

Key Takeaways:

- The policy rate remains unchanged, while the Fed's rhetoric remains cautious;

- Monetary policy remains moderately restrictive;

- U.S. macroeconomic data continue to support a soft-landing scenario: inflation risks are increasing, the labor market is cooling without signs of recession, and current conditions do not yet warrant a rate cut.

INFLATION: CONSUMER PRICE INDEX (MAY):

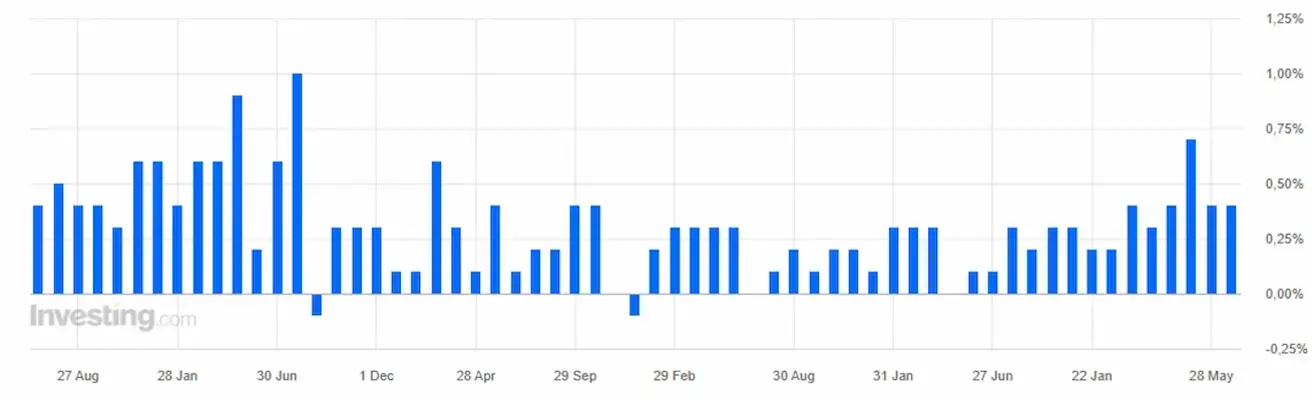

- Core CPI (MoM): 0.2% (previous: 0.4%).

- Core CPI (YoY): 2.9% (previous: 2.8%).

- CPI (MoM): 0.5% (previous: 0.6%).

- CPI (YoY): 4.2% (previous: 3.8%).

PRODUCER PRICE INDEX (MAY):

- PPI (MoM): 1.1% (previous: 1.4%).

- Core PPI (MoM): 0.4% (previous: 1.0%).

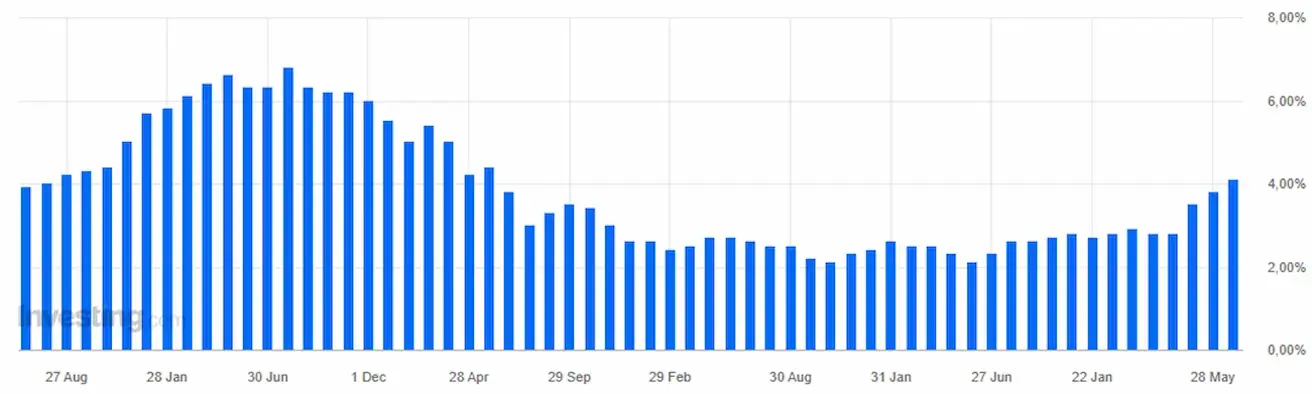

INFLATION EXPECTATIONS (MICHIGAN) (JUNE):

- 12-month Inflation Expectations: 4.6% (previous: 4.8%).

- 5-Year Inflation Expectations: 3.3% (previous: 3.9%).

Core Personal Consumption Expenditures (PCE) Price Index (May): YoY: 3.4% (prior: 3.3%); MoM: 0.3% (prior: 0.3%).

Headline Personal Consumption Expenditures (PCE) Price Index (May): YoY: 4.1% (prior: 3.8%); MoM: 0.4% (prior: 0.4%).

GDP (U.S. Bureau of Economic Analysis, BEA) — Q1 2025 annualized growth rate, third estimate: +2.1% (Q4 2025: +0.5%); forecast: +1.6%; second estimate: 2.0%.

GDPNow (the Atlanta Fed's real-time estimate of official GDP growth ahead of release): 2.5% (previous: 3.0%).

BUSINESS ACTIVITY INDEX (PMI) (MAY): (Above 50 indicates expansion; below 50 indicates contraction)

- Services PMI: 51.3 (previous: 50.7).

- Manufacturing PMI: 55.7 (previous: 55.1).

- Composite PMI: 52.2 (previous: 51.5).

LABOR MARKET (BLS) (MAY)

- Unemployment Rate: 4.3% (previous: 4.3%).

- Continued Jobless Claims: 1.821K (previous: 1.810K).

- Initial Jobless Claims: 227K (previous: 226K).

- Nonfarm Payrolls (NFP): 172K (previous: 179K).

- Private Nonfarm Payrolls: 120K (previous: 177K).

- Average Hourly Earnings (YoY): 3.4% (previous: 3.6%).

- JOLTS Job Openings: 6.866 million (previous: 6.922 million).

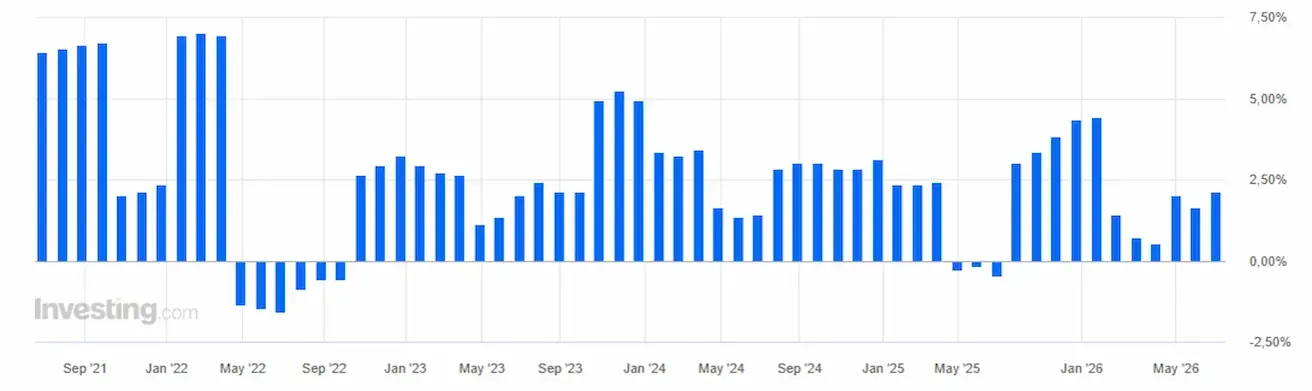

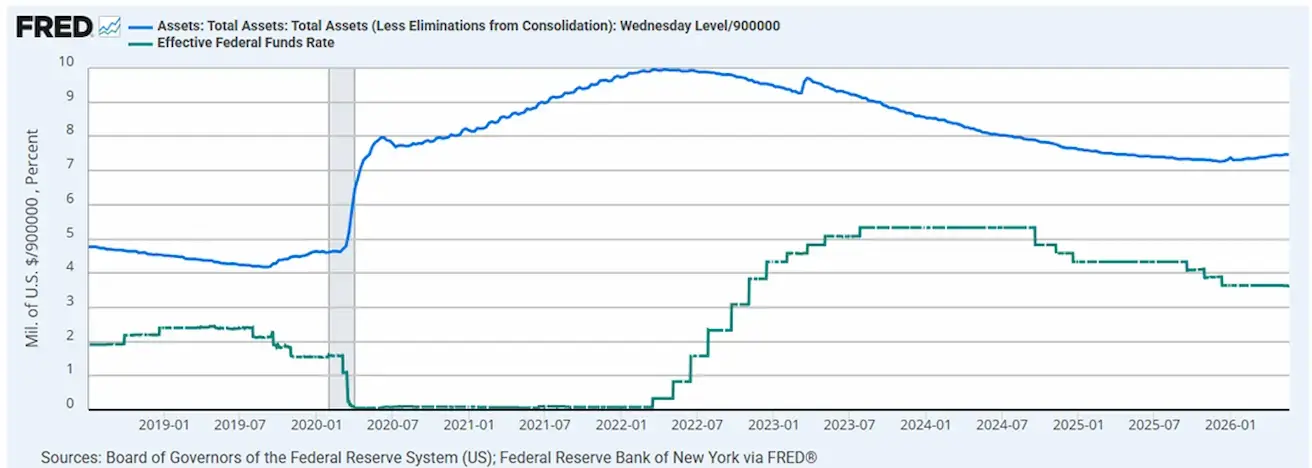

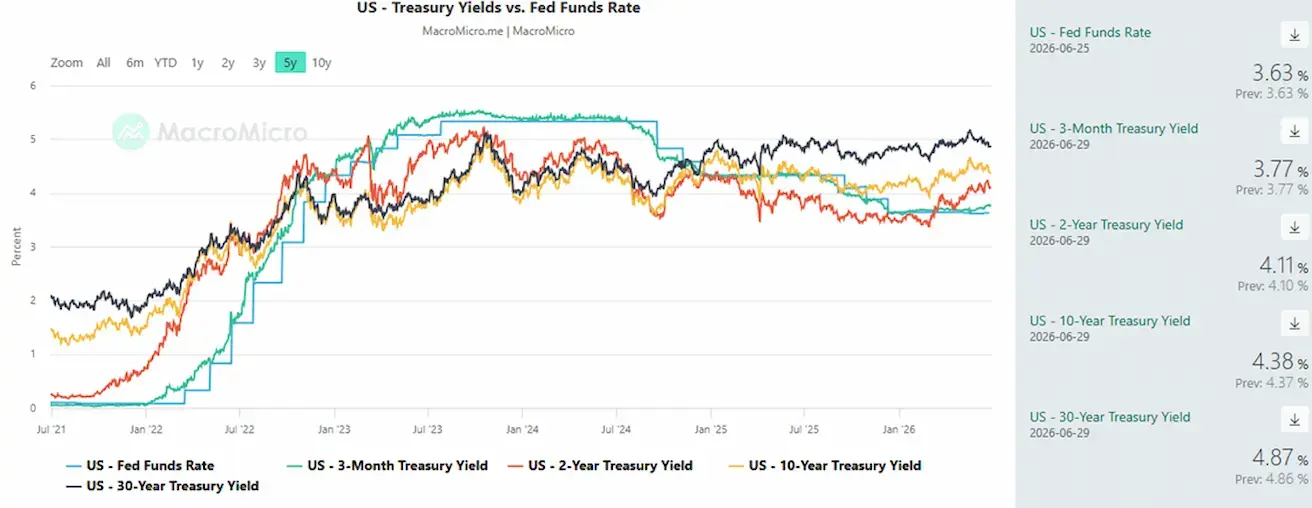

MONETARY POLICY

Effective Federal Funds Rate (EFFR): 3.50%–3.75%.

Federal Reserve Balance Sheet: $6.735 trillion, up 3.06% since the suspension of quantitative tightening (QT), when the balance sheet stood at $6.535 trillion.

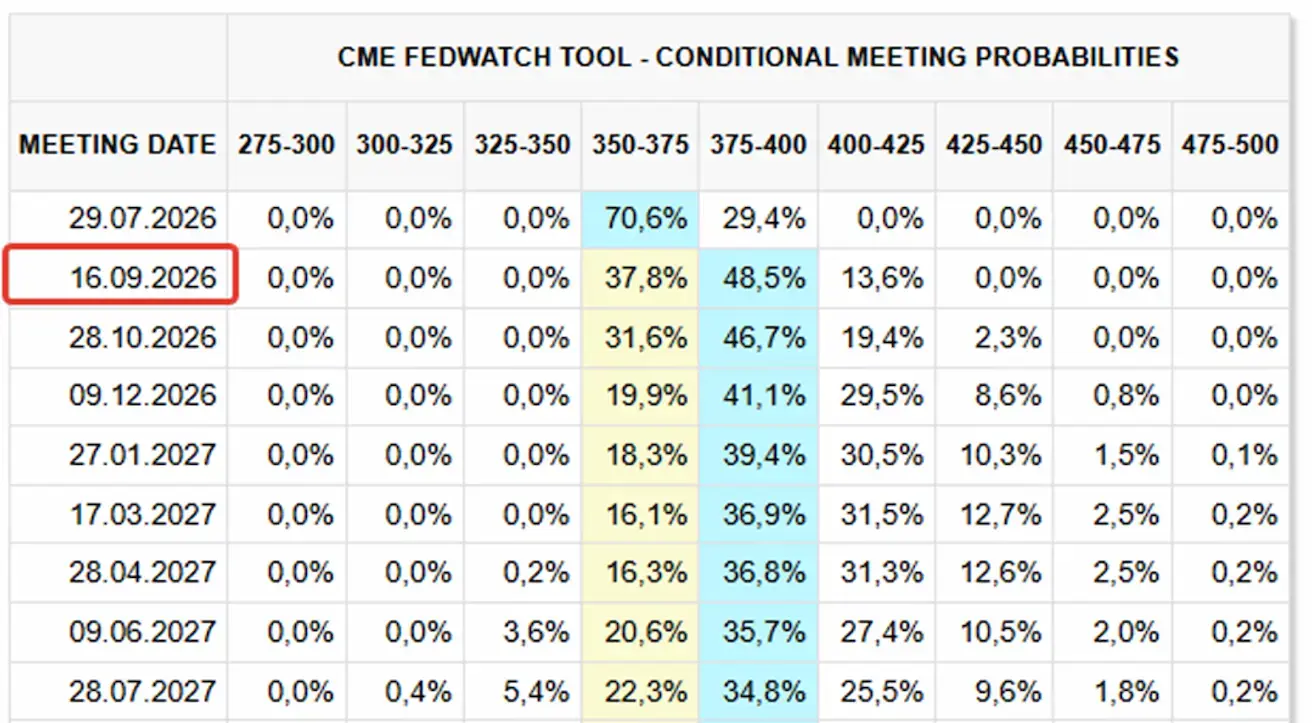

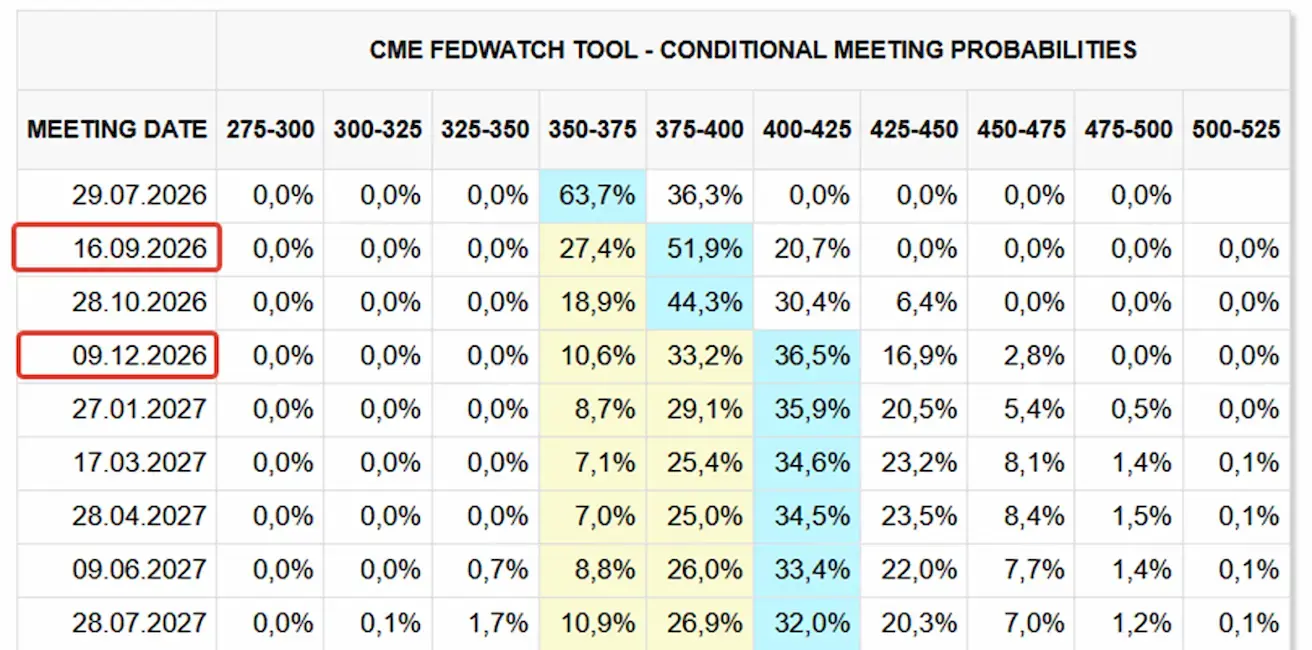

MARKET FORECAST FOR RATE (FEDWATCH)

For the next FOMC meeting (July 29), the implied market probability of a rate hike stands at 29.4% (week ago: 36.34%).

Over the next 12 months, the market is pricing in one 25-basis-point rate hike, bringing the federal funds rate to a target range of 4.00–4.25%, in September this year.

Today:

A week earlier:

Market

SP500

Weekly performance: -1,95% (week-end close: 7354,03); year-to-date: +7,43%.

NASDAQ100

Weekly performance: -4,24% (week-end close: 29118,24); year-to-date: +15,32%.

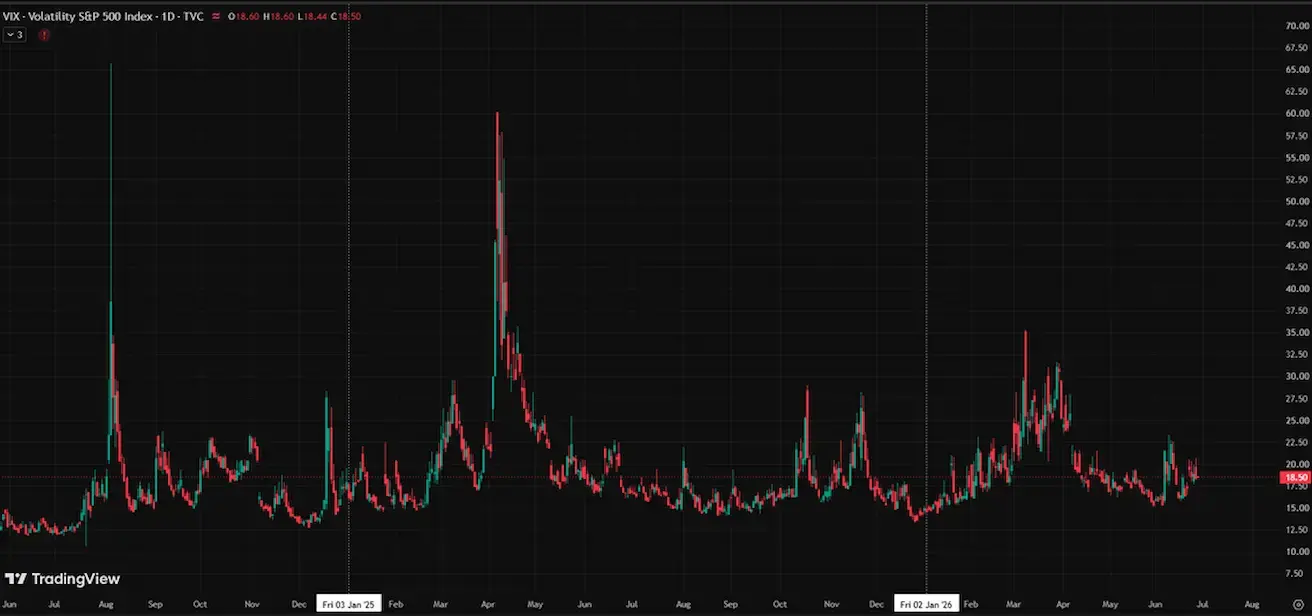

VIX

VIX (volatility index): week closing at 18,49 points.

Eurozone

- The ECB raised interest rates, while maintaining a hawkish stance as inflationary risks continue to increase;

- Against the backdrop of the conflict in the Middle East, the ECB revised its GDP forecasts downward and raised its inflation projections for the coming years.

Interest Rates

- Deposit Facility Rate: 2.25% (previous: 2.0%);

- Marginal Lending Facility Rate: 2.65% (previous: 2.4%) — the rate at which banks can obtain overnight funding from the central bank;

- Main Refinancing Rate (Policy Rate): 2.40% (previous: 2.15%).

ECB Communication

Inflation: Consumer Price Index (CPI) (May)

- Core CPI (YoY): 2.6% (previous: 2.2%);

- Headline CPI: 0.1% (MoM) (previous: 1.0%); 3.2% (YoY) (previous: 3.0%).

GDP (Q1 Preliminary Estimate)

- QoQ: -0.2% (previous: 0.1%);

- YoY: 0.3% (previous: 1.2%).

Unemployment Rate (May)

- 6.3% (previous: 6.3%).

Industrial Production (April)

- MoM: 0.1% (previous: 0.9%);

- YoY: 1.67% (previous: 1.37%).

Purchasing Managers' Index (PMI) (May)

- Services PMI: 48.9 (previous: 47.7);

- Manufacturing PMI: 51.3 (previous: 51.8);

- S&P Global Composite PMI: 49.5 (previous: 48.5).

EURO STOXX 600 (FXXP1!)

Weekly performance: +0,09% (week-end close: 638,5); year-to-date: +7,49%.

China

China's economy continues to stabilize, supported by strong export performance, while domestic demand and investment are gradually recovering. Policymakers remain measured and targeted in their approach to economic stimulus.

- Interest rates remain unchanged;

- Monetary policy remains accommodative;

- China reaffirmed its commitment to fiscal support for economic growth under its 2026 plan, including measures to stimulate domestic demand, optimize tax incentives and subsidies, and modernize industrial capacity.

Interest Rates

- 1-Year Loan Prime Rate (medium-term lending): 3.00%;

- 5-Year Loan Prime Rate (benchmark for mortgage lending): 3.50%.

Inflation Indicators (May)

- Consumer Price Index (CPI): -0.1% MoM (previous: 0.3%); 1.2% YoY (previous: 1.3%);

- Producer Price Index (PPI): 3.9% YoY (previous: 2.8%).

Trade Data (May)

- Imports: 27.4% YoY (previous: 25.3%);

- Exports: 19.4% YoY (previous: 14.1%);

- Trade Balance (USD): $105.43 billion (previous: $84.80 billion).

GDP (Q1 2026)

- QoQ: 1.3% (previous: 1.2%);

- YoY: 5.0% (previous: 4.5%).

Labor Market

- Unemployment Rate (May): 5.1% (previous: 5.2%).

Industrial Activity

- Industrial Production (May, YoY): 4.5% (previous: 4.1%).

Fixed Asset Investment

- May, YoY: -4.1% (previous: -1.6%).

Retail Sales

- April, YoY: 0.9% (previous: 1.3%).

Purchasing Managers' Indices (PMI) (May)

- Manufacturing PMI: 50.0 (previous: 50.3);

- Non-Manufacturing PMI: 50.1 (previous: 49.4);

- Composite PMI: 50.5 (previous: 50.1).

CSI 300 INDEX (000300.HK)

Weekly performance: -0,30% (week-end close: 4626,921); year-to-date: +5,69%.

BOND MARKET

U.S. Treasury Bonds 20+ Years (TLT ETF): +0,68% for the week (weekly close: 87,34); +0,21% year-to-date.

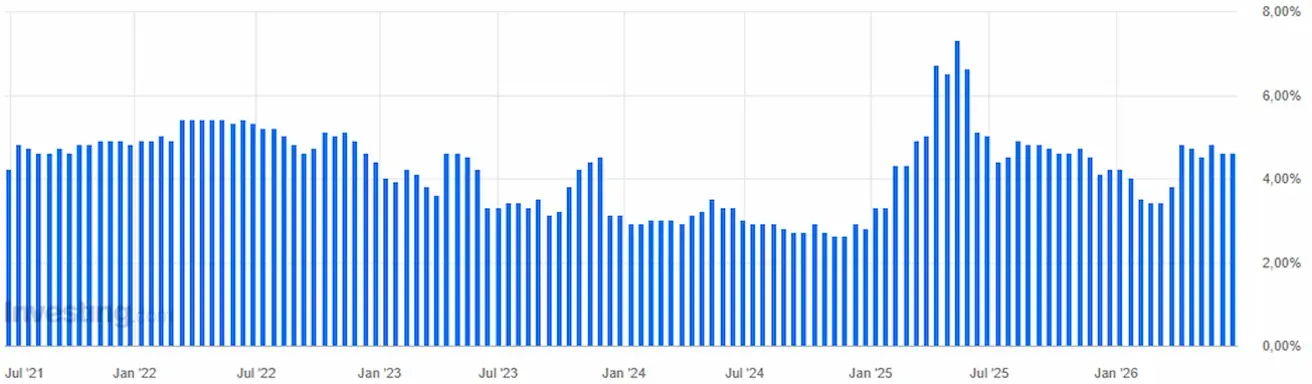

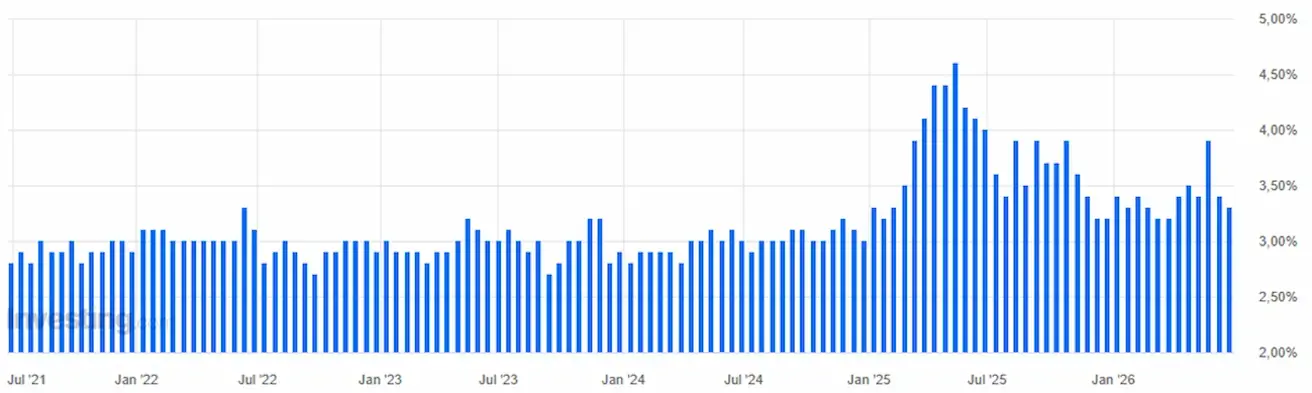

YIELDS AND SPREADS

- Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity: 4.38% (previous: 4.49%);

- 2-Year U.S. Treasury Yield: 4.11% (previous: 4.22%);

- ICE BofA BBB US Corporate Index Effective Yield: 5.31% (previous: 5.39%).

- The yield spread between 10-year and 2-year U.S. Treasury securities stands at 27 basis points (previous: 27 bps);

- The yield spread between 10-year and 3-month U.S. Treasury securities stands at 61 basis points (previous: 72 bps).

The cost of a 5-year U.S. Credit Default Swap (CDS) — a market-based measure of sovereign default insurance — rose to 38.21 basis points, compared with 39.22 basis points a week earlier.

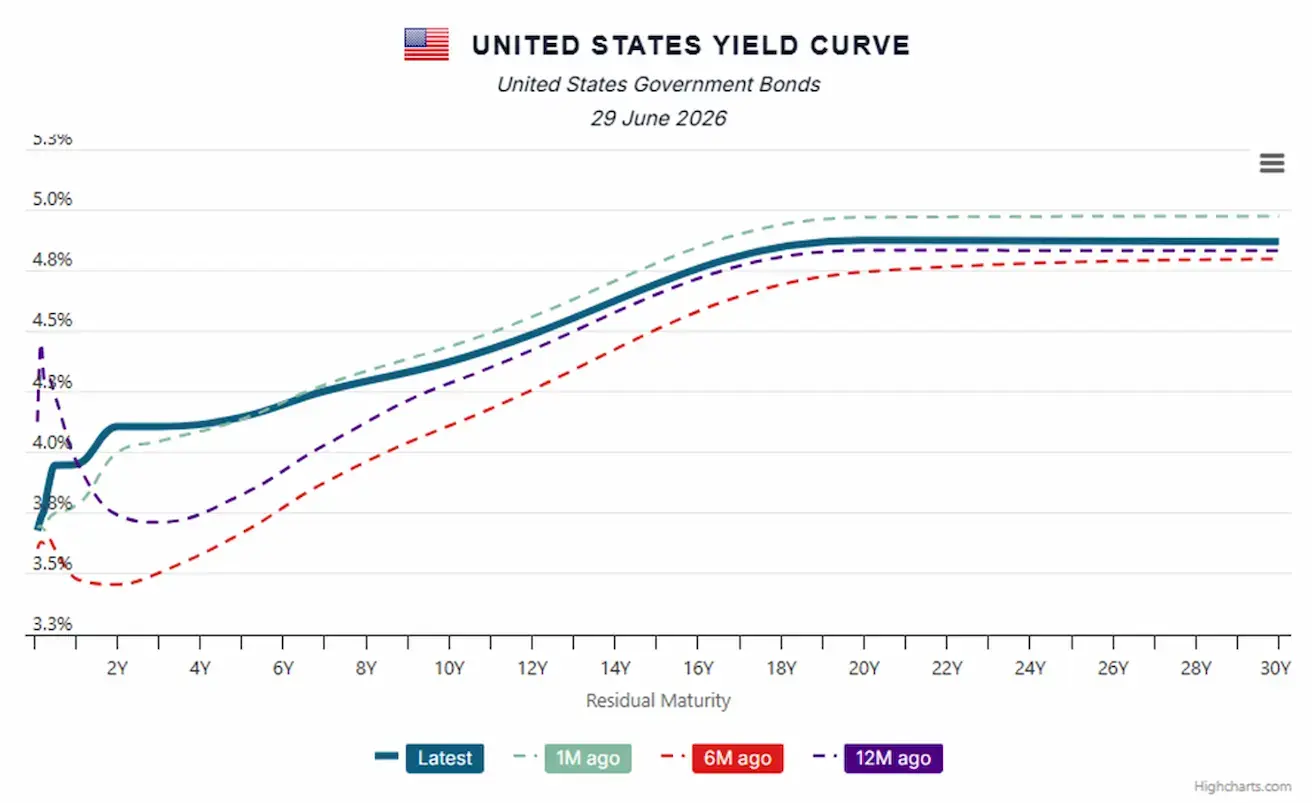

U.S. Treasury Yield Curve:

GOLD FUTURES (GC)

Weekly performance: -1,59% (week close: $4095,8 per troy oz); year-to-date: -5,45%

OIL FUTURES

Weekly performance: -8,73% (week close: $69,23 per barrel); year-to-date: +20,59%

DOLLAR INDEX FUTURES (DX)

Weekly performance: +0,58% (week close: 101,082); year-to-date: +3,15%.

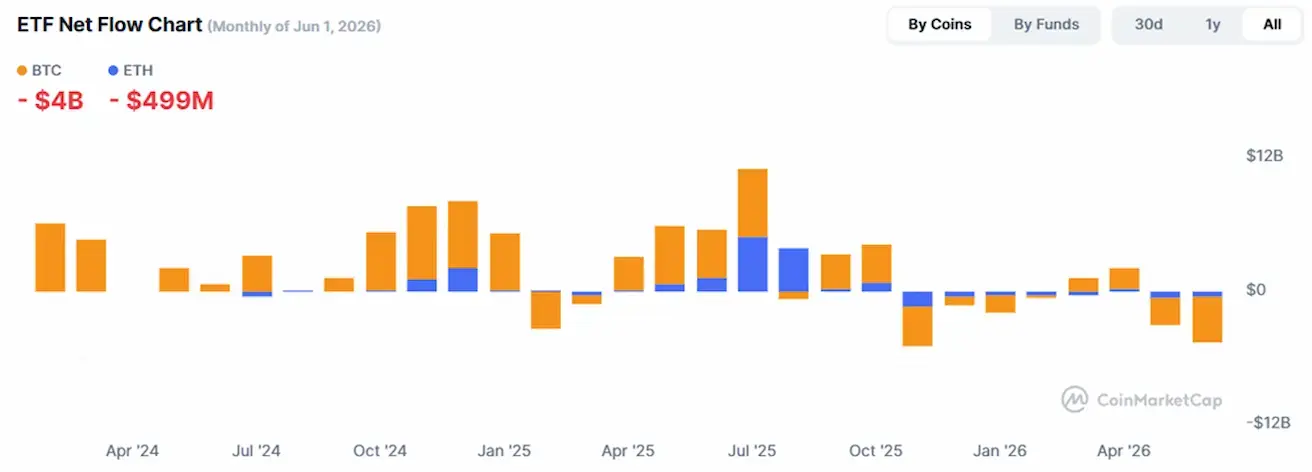

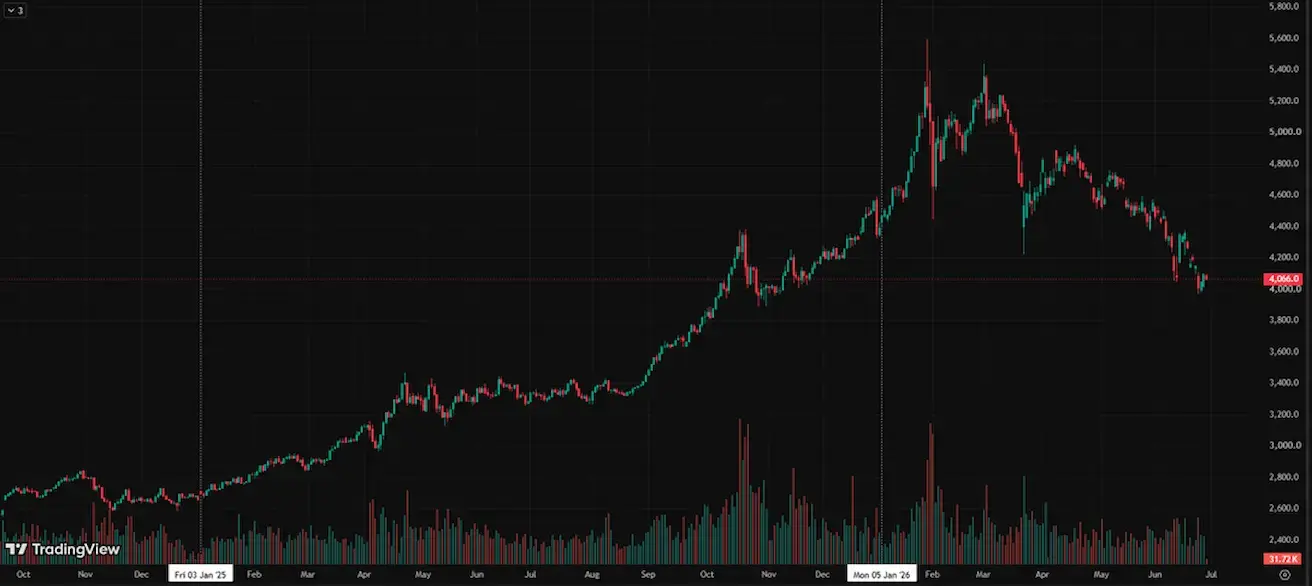

BTC FUTURES

Weekly performance: -5,95% (week close: $59474,01); year-to-date: -32,20%.

ETH FUTURES

Weekly performance: -7,94% (week close: $1596,41); year-to-date: -47,23%.

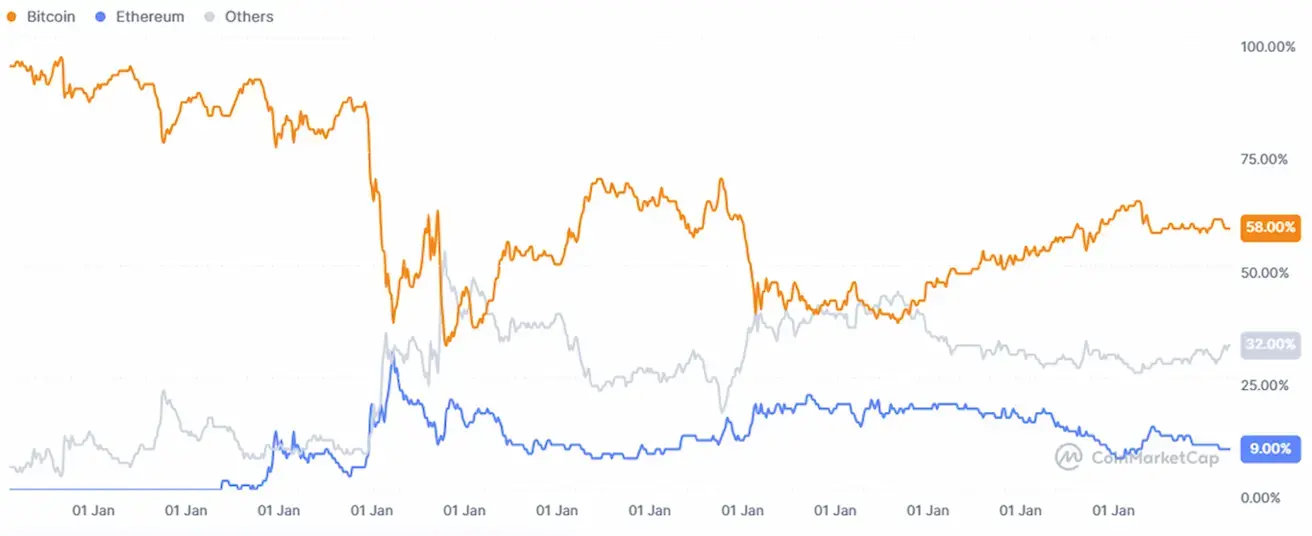

TOTAL CRYPTOCURRENCY MARKET CAPITALIZATION

Total crypto market capitalization: $2,08 trillion (vs $2,20 trillion a week earlier) (coinmarketcap.com).

Crypto asset market shares:

- Bitcoin 58,10% (prev. 58,40%)

- Ethereum 9,20% (prev. 9,60%)

- Others 32,7% (prev. 32,1%)

ETF Net Flows Chart: