Lietuvių

Lietuvių Русский

Русский Қазақша

Қазақша Eesti

EestiJune 28 – July 6, 2026: Weekly economic update

Key market updates

Key Takeaways:

- The policy rate remains unchanged, while the Fed’s rhetoric remains cautious;

- monetary policy remains moderately restrictive;

- U.S. macroeconomic data continue to support a soft-landing scenario: inflation risks are increasing, the labor market is cooling without signs of recession, and current conditions do not yet warrant a rate cut.

The unemployment rate decreased, while new claims for insurance benefits increased slightly but remained near record lows. Meanwhile, the volume of ongoing recipients remained stable. These indicators imply that the broader economy is currently avoiding significant workforce reductions.

At the same time, the rate of employment growth has decelerated significantly, suggesting greater corporate hesitation about adding to the workforce.

Broadly, employment dynamics continue to align with a soft-landing thesis. While specific metrics provide divergent signals, aggregate data indicate a measured deceleration in labor demand, avoiding an abrupt contraction. This scenario aligns with the Fed’s expectations and reduces the likelihood of both a further rate hike and a sharp deterioration in economic conditions. For the equity market, this combination of factors remains favorable.

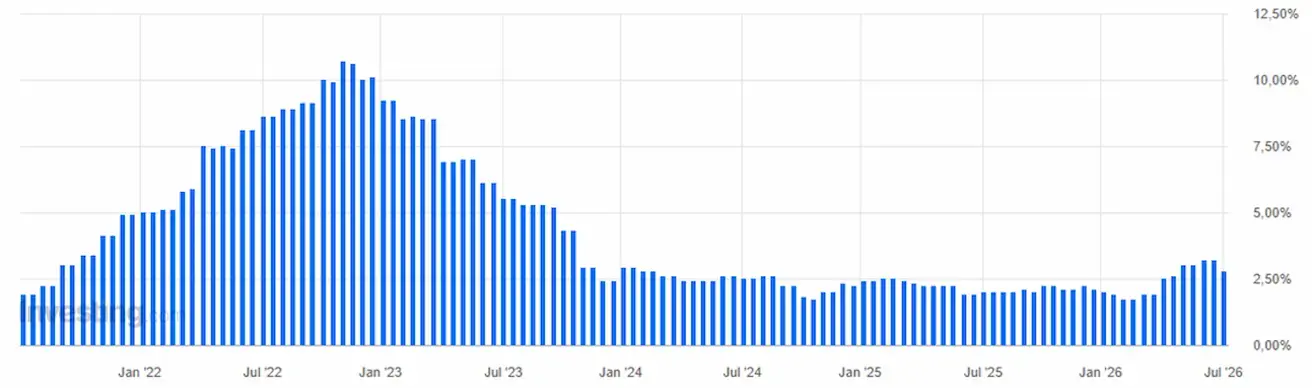

Inflation: Consumer Price Index (May)

- Core CPI (MoM): 0.2% (previous: 0.4%);

- Core CPI (YoY): 2.9% (previous: 2.8%);

- CPI (MoM): 0.5% (previous: 0.6%);

- CPI (YoY): 4.2% (previous: 3.8%).

Producer Price Index (May)

- PPI (MoM): 1.1% (previous: 1.4%);

- Core PPI (MoM): 0.4% (previous: 1.0%).

Inflation Expectations (Michigan) (June)

- 12-month inflation expectations: 4.6% (previous: 4.8%);

- 5-year inflation expectations: 3.3% (previous: 3.9%).

GDP (U.S. Bureau of Economic Analysis, BEA): Q1 2025 annualized growth rate, third estimate — +2.1% (Q4 2025: +0.5%); forecast: +1.6%; second estimate: 2.0%.

GDPNow (the Atlanta Fed’s real-time estimate of official GDP growth ahead of its release): 1.2% (previous: 2.5%).

Labor Market (BLS) (May)

- Unemployment rate: 4.2% (previous: 4.3%);

- continued jobless claims: 1,814K (previous: 1,812K);

- initial jobless claims: 215K (previous: 216K);

- nonfarm payrolls (NFP): 57K (previous: 129K);

- private nonfarm payrolls: 49K (previous: 97K);

- average hourly earnings (YoY): 3.5% (previous: 3.4%);

- JOLTS job openings: 6.866 million (previous: 6.922 million).

Purchasing Managers’ Index (PMI) (May)

Above 50 indicates expansion; below 50 indicates contraction.

- Services PMI: 51.3 (previous: 50.7);

- Manufacturing PMI: 53.9 (previous: 55.1);

- Composite PMI: 52.2 (previous: 51.5).

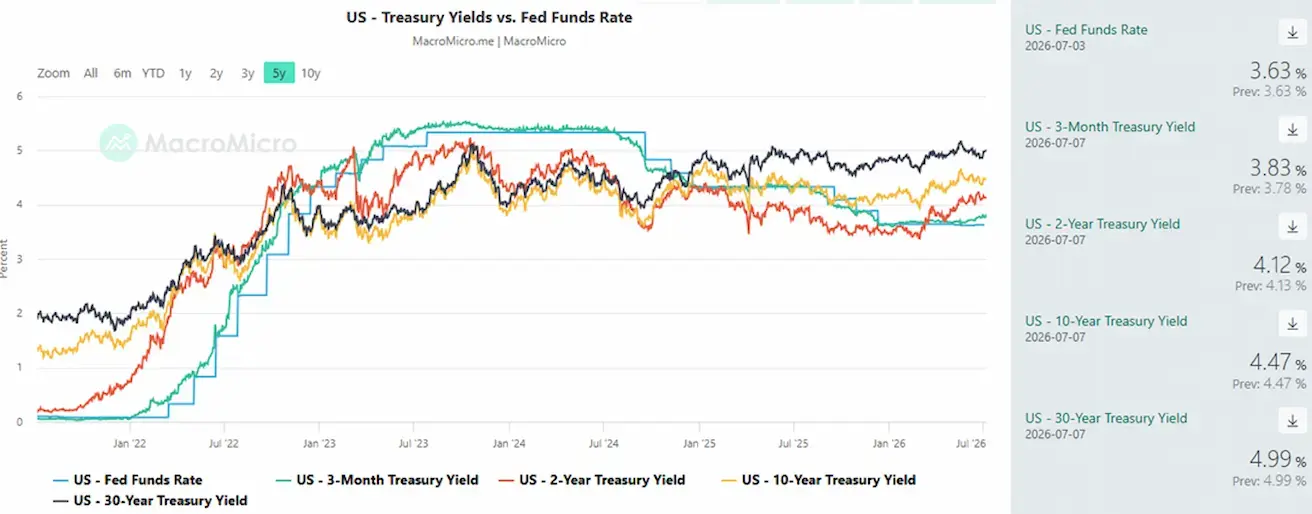

Monetary Policy

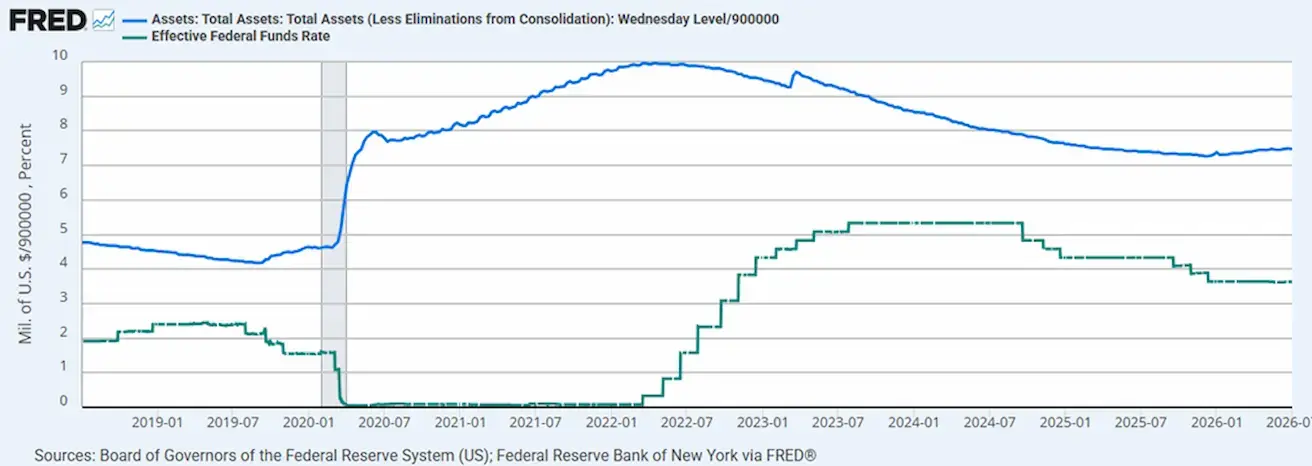

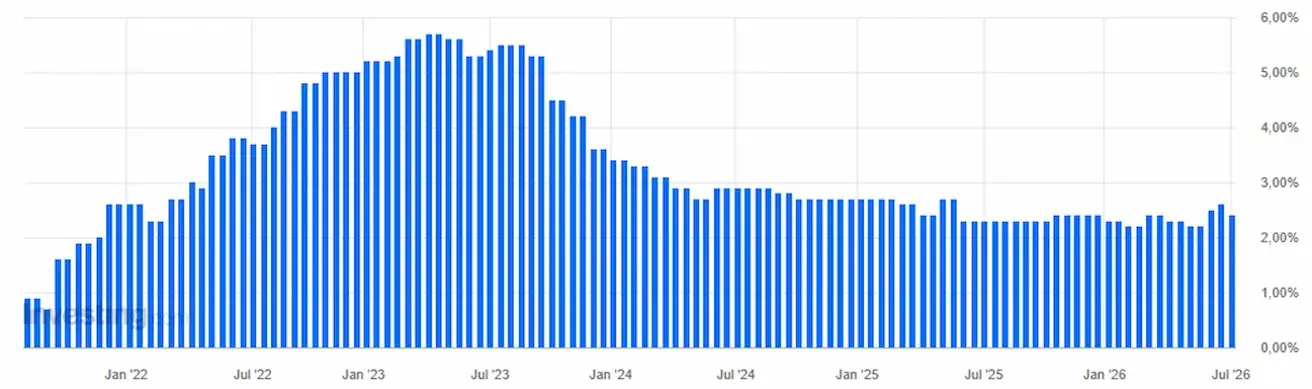

Effective Federal Funds Rate (EFFR): 3.50%–3.75%.

Federal Reserve balance sheet: $6.724 trillion, +2.89% since the suspension of quantitative tightening (QT), when the balance sheet stood at $6.535 trillion.

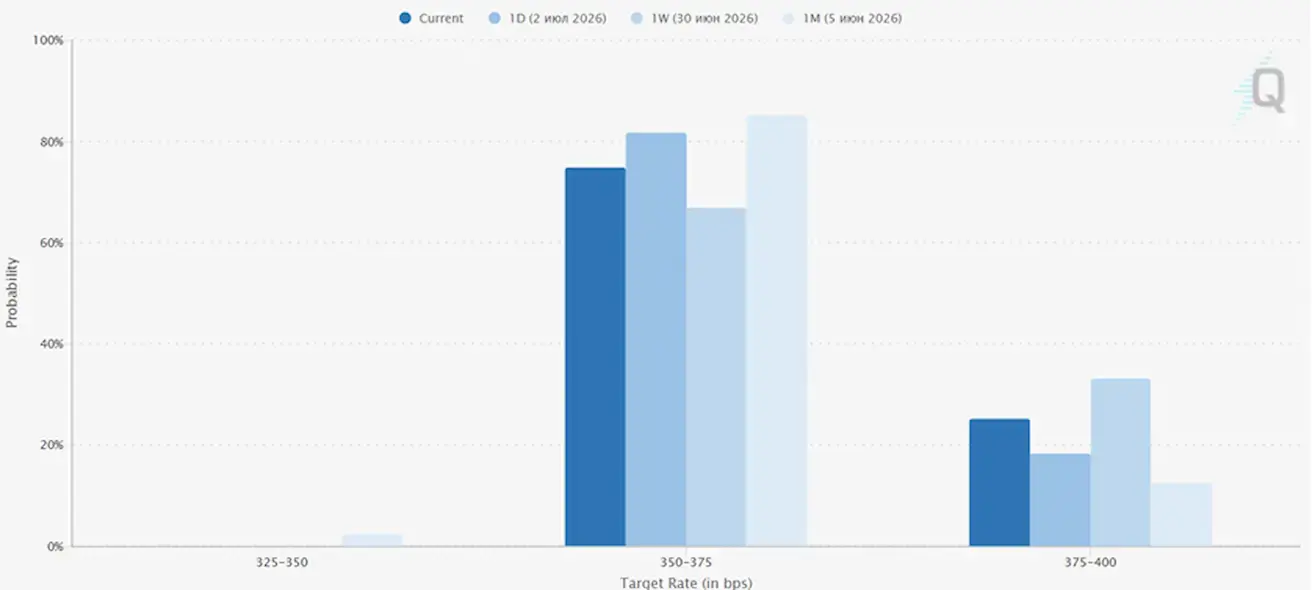

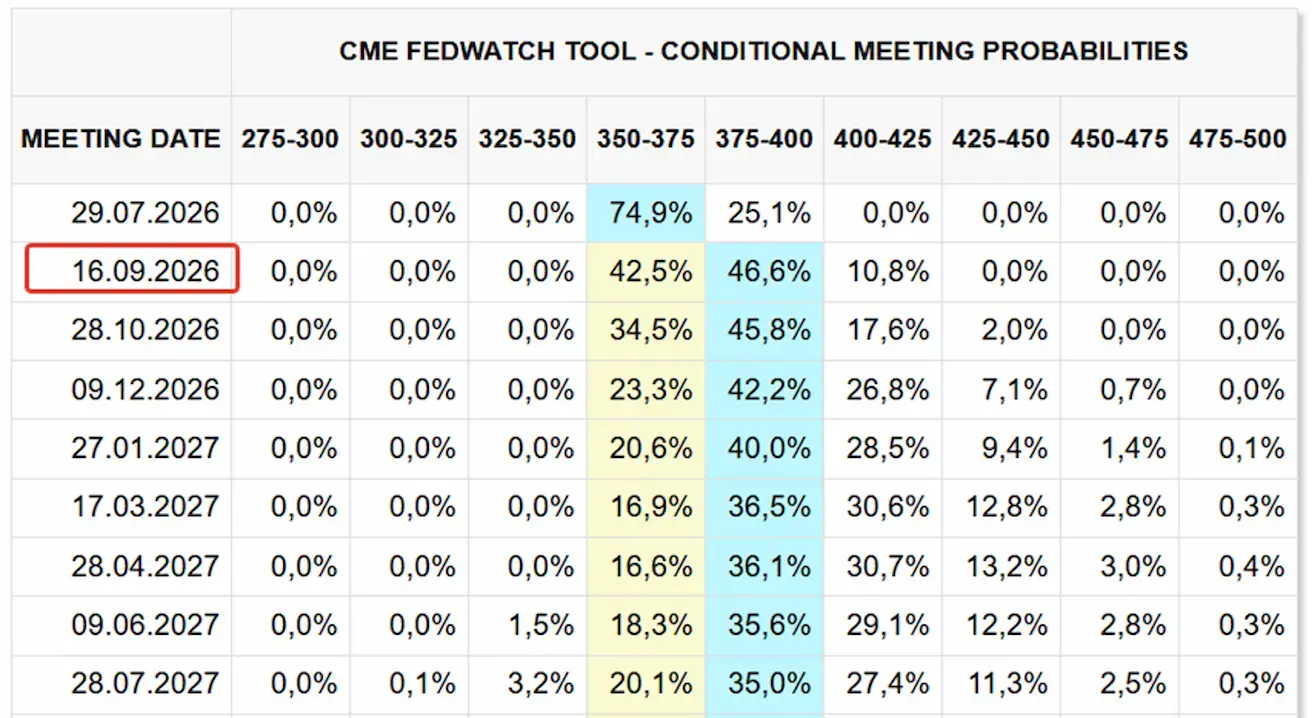

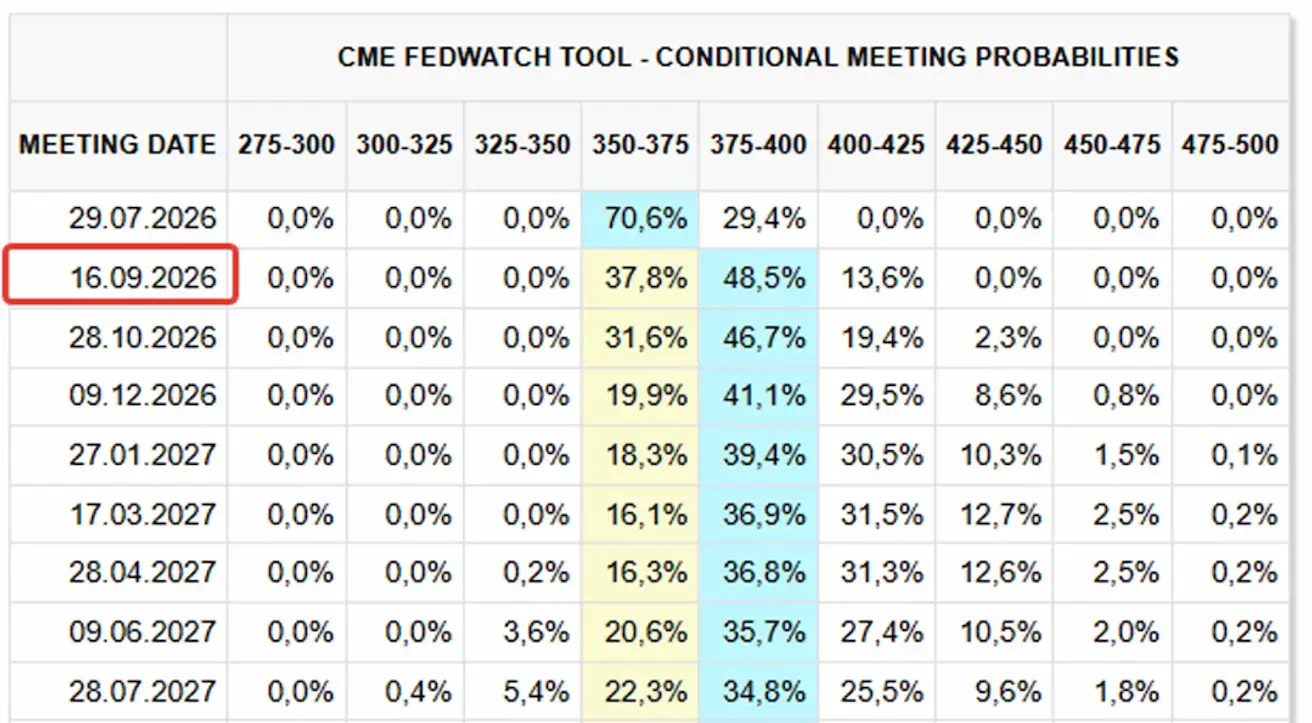

Fedwatch

- For the next FOMC meeting (July 29), the implied market probability of a rate hike has declined to 25.1% (a week ago: 29.4%).

Over the next 12 months, the market is pricing in one 25-basis-point rate hike in September this year, bringing the federal funds rate to a target range of 4.00–4.25%.

Today:

A week earlier:

Market

SP500

Weekly performance (including July 6): +2.42% (week-end close: 7,537.42); year-to-date: +10.11%.

Nasdaq100

Weekly performance (including July 6): +1.99% (week-end close: 29,697.87); year-to-date: +17.62%.

VIX

VIX (volatility index): July 6 closing at 15.56 points.

Wall Street enters the second week of July with focus shifting to the start of second-quarter earnings season.

SpaceX (SPCX) also remains in the spotlight following its IPO. The analyst quiet period on the company’s stock expires this week, and in the coming weeks we can expect coverage initiations from Goldman Sachs, Morgan Stanley, JPMorgan, BofA, Citi, and other members of the IPO syndicate. That is when a full market consensus on the target price and valuation will take shape.

Today, July 7, 2026, SpaceX (SPCX) officially joined the Nasdaq-100 ahead of the main trading session’s open. As of today, SpaceX is a full-fledged index component, and all funds tracking the Nasdaq-100 are now required to hold its shares in their portfolios.

With the Nasdaq-100 inclusion catalyst now fully realized, subsequent market movements will be increasingly dictated by underlying corporate fundamentals and upcoming consensus valuations from syndicate analysts.

Eurozone

- The ECB raised interest rates, while maintaining a hawkish stance as inflationary risks continue to increase;

- Against the backdrop of the conflict in the Middle East, the ECB revised its GDP forecasts downward and raised its inflation projections for the coming years.

Eurozone inflation continues to gradually ease, while the economy is showing signs of stabilization. Despite weak GDP growth at the start of the year, the labor market remains resilient (unemployment rate at 6.2%), and business activity has returned to neutral territory (the S&P Global Composite Index came in at 50).

The Euro Stoxx 600 has climbed to new local highs. At the same time, ECB officials continue to maintain a moderately hawkish tone, as core inflation still exceeds the target, though a consensus is now forming for just one further rate hike.

Interest Rates

- Deposit facility rate: 2.25% (previous: 2.0%);

- marginal lending facility rate: 2.65% (previous: 2.4%) — the rate at which banks can obtain overnight funding from the central bank;

- main refinancing rate (policy rate): 2.40% (previous: 2.15%).

Inflation: Consumer Price Index (CPI) (May)

- Core CPI (YoY): 2.4% (previous: 2.6%);

- Headline CPI: -0.1% (MoM) (previous: 0.1%); 2.8% (YoY) (previous: 3.2%).

According to Eurostat’s flash estimate, annual eurozone inflation in June 2026 is expected to be 2.8%, down from 3.2% in May. Core CPI also declined by 0.2 percentage points to 2.4%.

Looking at the main components of eurozone inflation, the highest annual rate in June is expected in the energy sector (8.7%, compared with 10.8% in May), followed by services (3.2%, compared with 3.5% in May), food, alcohol and tobacco (1.6%, compared with 1.9% in May), and non-energy industrial goods (0.9%, stable compared with May).

GDP (Q1 Preliminary Estimate)

- QoQ: -0.2% (previous: 0.1%);

- YoY: 0.3% (previous: 1.2%).

Unemployment Rate (May)

6.2% (previous: 6.3%).

Industrial Production (May)

- MoM: 0.1% (previous: 0.9%);

- YoY: 1.67% (previous: 1.37%).

Purchasing Managers’ Index (PMI) (May)

- Services PMI: 49.4 (previous: 47.7);

- Manufacturing PMI: 51.4 (previous: 51.6);

- S&P Global Composite PMI: 50.0 (previous: 48.5).

Euro Stoxx 600 (FXXP1!)

Weekly performance (including July 6): +2.18% (week-end close: 652.4); year-to-date: +9.83%.

China

China’s economy continues to stabilize, supported by strong export performance, while domestic demand and investment are gradually recovering. Policymakers remain measured and targeted in their approach to economic stimulus.

- Interest rates remain unchanged;

- monetary policy remains accommodative;

- China reaffirmed its commitment to fiscal support for economic growth under its 2026 plan, including measures to stimulate domestic demand, optimize tax incentives and subsidies, and modernize industrial capacity.

Interest Rates

- 1-year loan prime rate (medium-term lending): 3.00%;

- 5-year loan prime rate (benchmark for mortgage lending): 3.50%.

Inflation Indicators (May)

- Consumer Price Index (CPI): -0.1% MoM (previous: 0.3%); 1.2% YoY (previous: 1.3%);

- Producer Price Index (PPI): 3.9% YoY (previous: 2.8%).

Trade Data (May)

- Imports: 27.4% YoY (previous: 25.3%);

- exports: 19.4% YoY (previous: 14.1%);

- trade balance (USD): $105.43 billion (previous: $84.80 billion).

GDP (Q1 2026)

- QoQ: 1.3% (previous: 1.2%);

- YoY: 5.0% (previous: 4.5%).

Labor Market

Unemployment rate (May): 5.1% (previous: 5.2%).

Industrial Activity

Industrial production (May, YoY): 4.5% (previous: 4.1%).

Fixed Asset Investment

May, YoY: -4.1% (previous: -1.6%).

Retail Sales

May, YoY: 0.9% (previous: 1.3%).

Purchasing Managers’ Index (PMI) (May)

- Manufacturing PMI: 50.3 (previous: 50.0);

- Non-Manufacturing PMI: 50.2 (previous: 50.1);

- Composite PMI: 50.6 (previous: 50.5).

CSI 300 Index (000300.HK)

Weekly performance: -1.72% (week-end close: 4,841.99); year-to-date: +3.87%.

Bond Market

U.S. Treasury Bonds 20+ Years (TLT ETF): +0.68% for the week (weekly close: 87.34); +0.21% year-to-date.

Yields and Spreads

- Market yield on U.S. Treasury securities at 10-year constant maturity: 4.47% (previous: 4.38%);

- 2-year U.S. Treasury yield: 4.12% (previous: 4.11%);

- ICE BofA BBB US Corporate Index effective yield: 5.38% (previous: 5.31%).

- The yield spread between 10-year and 2-year U.S. Treasury securities stands at 35 basis points (previous: 27 bps);

- The yield spread between 10-year and 3-month U.S. Treasury securities stands at 64 basis points (previous: 61 bps).

The cost of a 5-year U.S. Credit Default Swap (CDS) — a market-based measure of sovereign default insurance — rose to 38.22 basis points, compared with 38.21 basis points a week earlier.

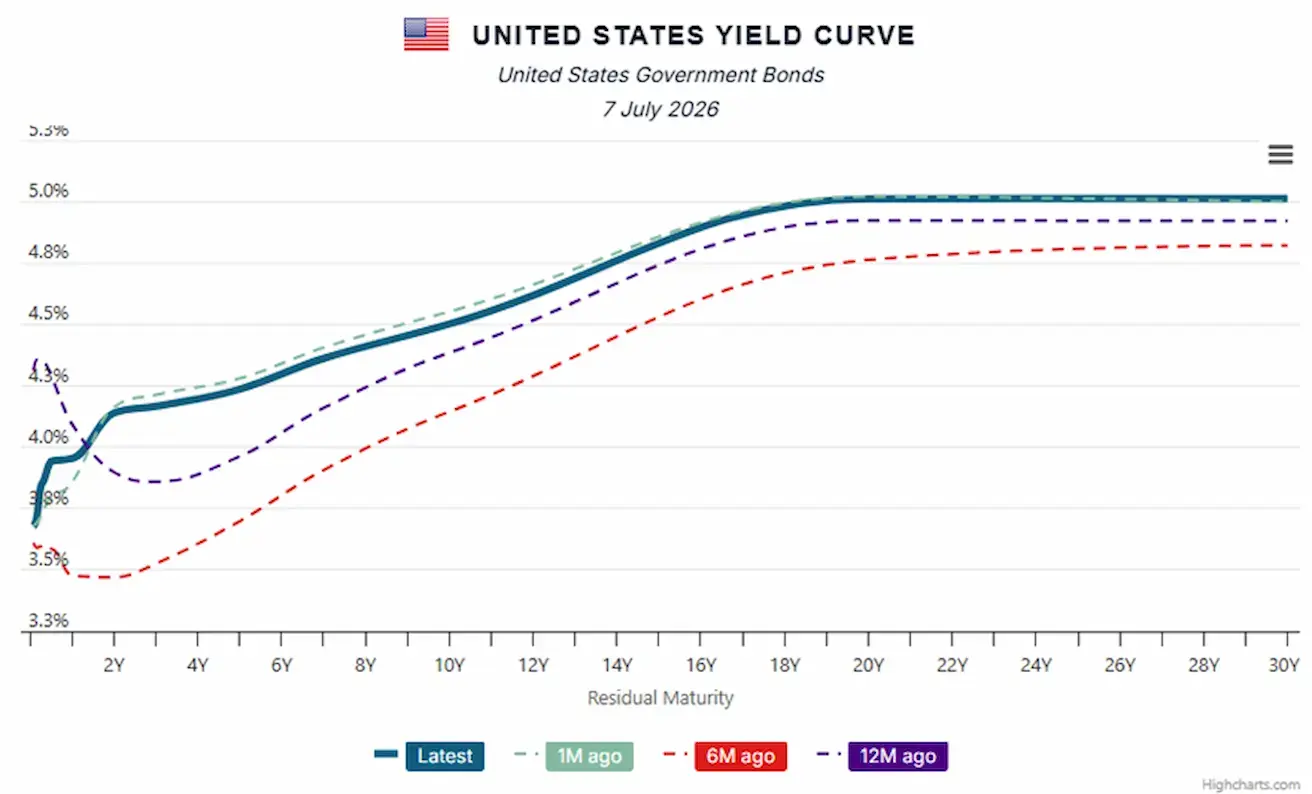

U.S. Treasury Yield Curve

The positive slope of the yield curve indicates that investor confidence in the resilience of the U.S. economy remains intact, with no signs of an imminent economic downturn.

Commodities

Gold Futures (GC)

Weekly performance: +1.69% (week close: $4,164.9 per troy oz); year-to-date: -3.86%.

Oil Futures

Weekly performance: -0.98% (week close: $68.55 per barrel); year-to-date: +19.40%.

OPEC+ continues to gradually ramp up production, with output set to rise by a further 188,000 barrels per day. The alliance’s next meeting is scheduled for August 2, when members will again assess the global market balance and the outlook for further supply increases.

The market has effectively shifted its focus from supply-shortage risk to the balance between supply and demand.

Several factors are currently at play:

- Much of the geopolitical premium has faded following de-escalation in the Middle East;

- OPEC+ is gradually restoring previously curtailed volumes to the market;

- demand remains steady but is not accelerating;

- inventories show no signs of a significant shortfall.

The gradual increase in output by major producers (OPEC+, the US, the UAE, which has left OPEC and holds substantial spare capacity) is driving oil prices lower, thereby easing inflationary pressure across the global economy. This is particularly significant for net energy-importing countries.

For central banks, the reduced risk of a new wave of inflation allows for a softer tone in policy communication, which is a positive factor for equity markets.

Dollar Index Futures (DX)

Weekly performance: -0.55% (week close: 100.527); year-to-date: +2.58%.

Cryptocurrencies

Bitcoin Futures

Weekly performance: +7.61% (week close: $64,001.84); year-to-date: -27.04%.

Ethereum Futures

Weekly performance: +14.59% (week close: $1,798.45); year-to-date: -39.53%.

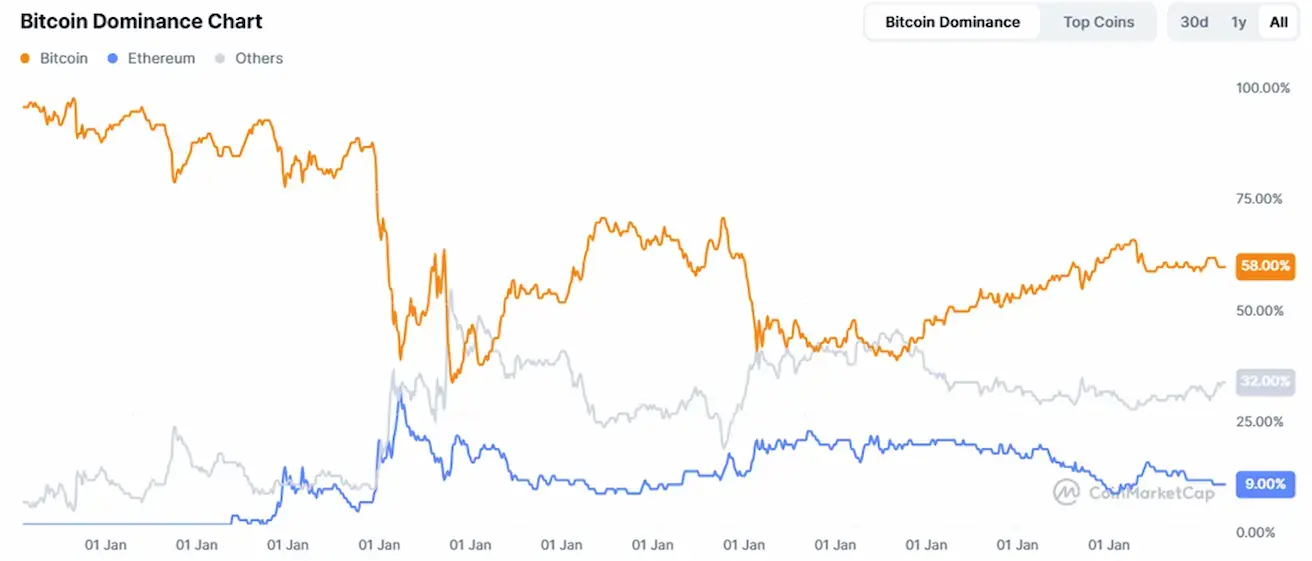

Total Cryptocurrency Market Capitalization

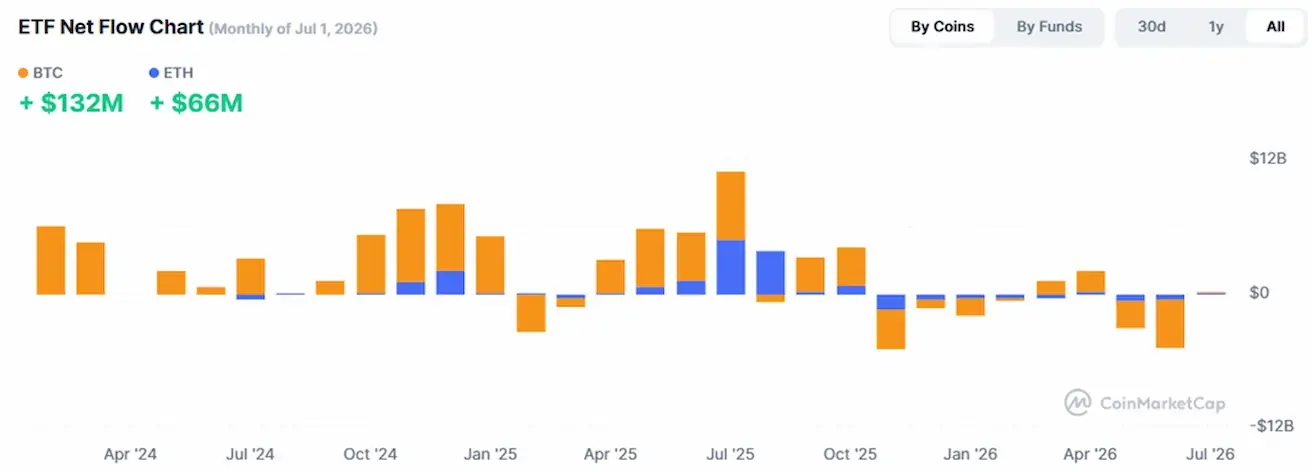

Total cryptocurrency market capitalization: $2.18 trillion (vs. $2.08 trillion a week earlier) (coinmarketcap.com).

Crypto asset market shares:

- Bitcoin: 58.1% (previous: 58.10%);

- Ethereum: 9.8% (previous: 9.20%);

- others: 32.1% (previous: 32.7%).

ETF net flows chart: