Lietuvių

Lietuvių Русский

Русский Қазақша

Қазақша Eesti

EestiVenture Capital Market: Q1 2026

Raison Analytical Review

Our analytical team has examined the data for the first quarter of 2026. The quarter proved exceptional across multiple metrics — both in investment volume and exit activity. Yet behind the record numbers lies a more nuanced picture: the market is becoming more concentrated, but it continues to grow.

The American Market

The figures below refer to the American venture market, which still accounts for 82% of the global market (including the US, Canada, and Latin America).

A Record Start and AI Dominance

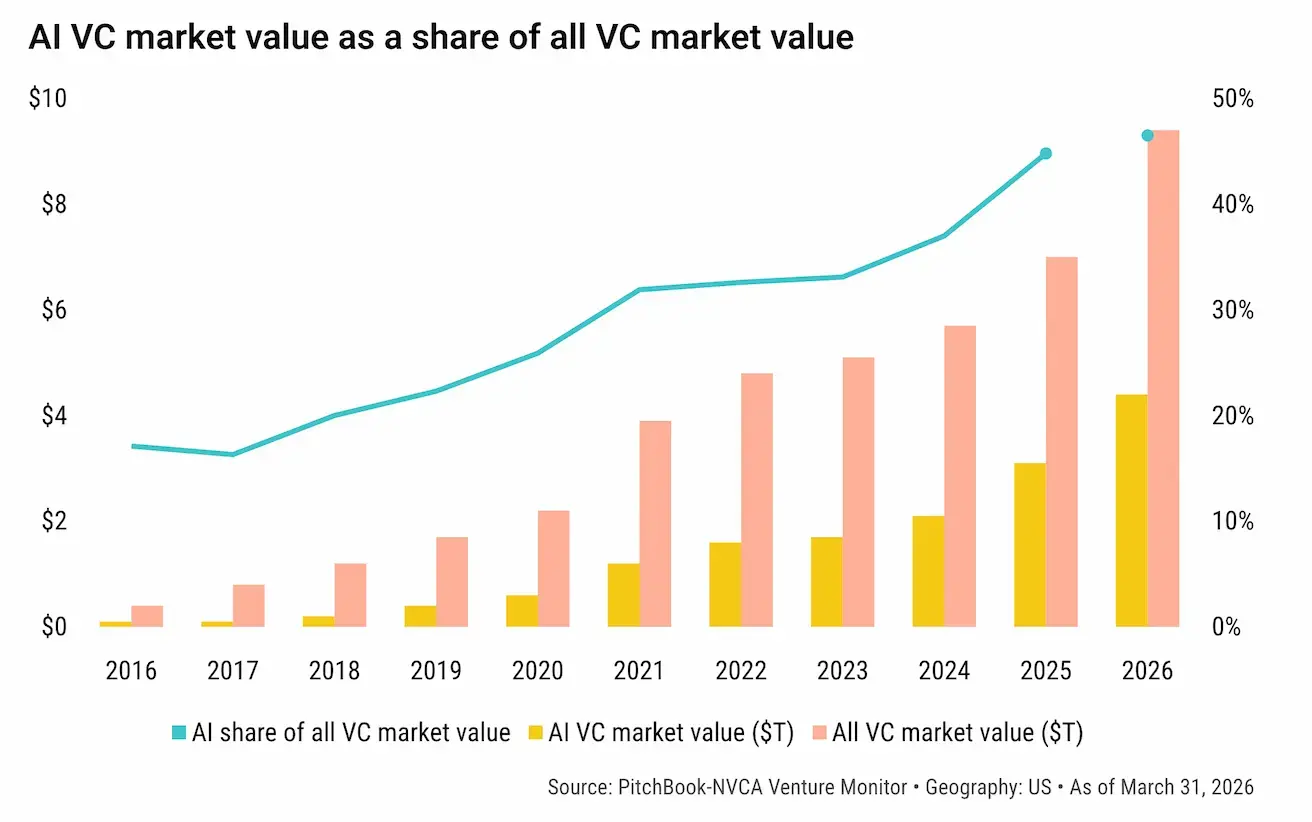

Q1 2026 became the most active investment quarter on record. The total venture market value reached $9.4 trillion — nearly half of which belongs to AI companies: $4.41 trillion, or 46.5% of the total. Just a few years ago, such a concentration of value in a single sector would have seemed like an exaggeration. Today, it is simply a market fact.

Chart: Total venture asset value by year.

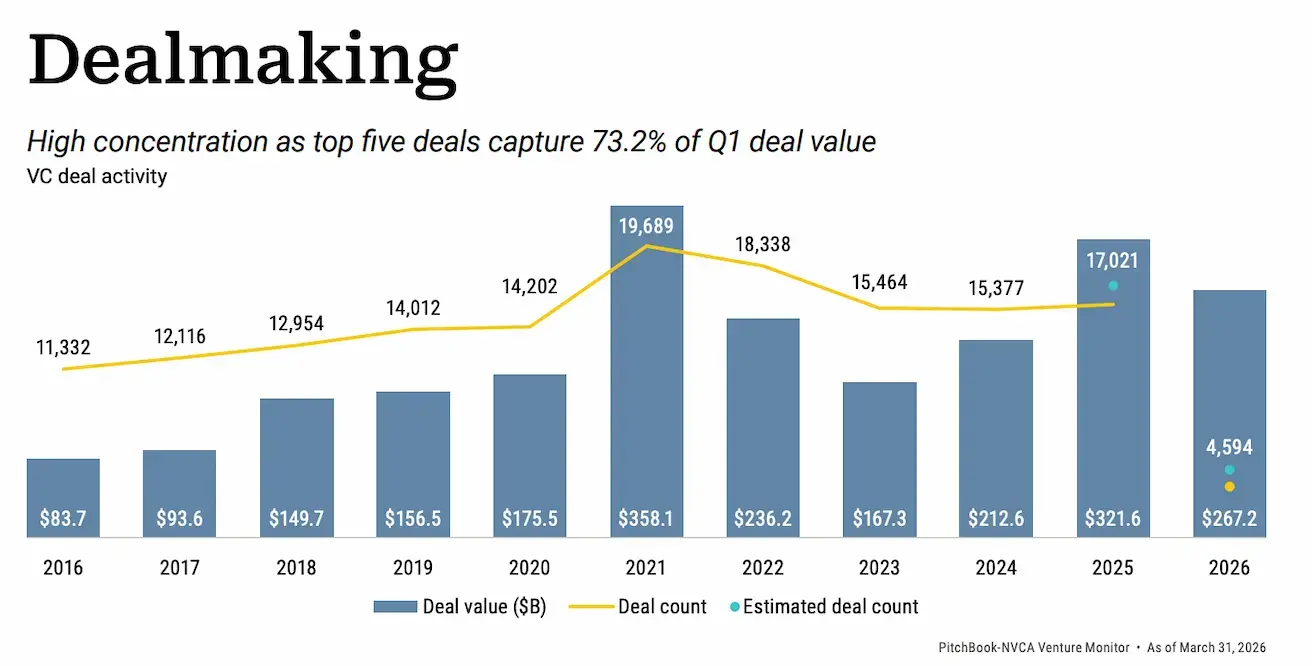

Capital Concentration in Five Deals

After just one quarter, 2026 has already claimed third place among the most active investment years of the past decade — behind only 2021 and 2025. Total Q1 investment volume reached $267.2 billion.

However, 73.2% of that figure came from just five deals:

- OpenAI — $122 billion

- Anthropic — $30 billion

- xAI — $20 billion

- Waymo — $16 billion

- Databricks — $5 billion

In total, $193 billion landed in the hands of five late-stage companies.

Chart: Investment volume and deal count by year over the past 10 years.

On one hand, this concentration inevitably raises a question: are massive AI rounds crowding out everything else? On the other hand, deal-count data offer a reassuring answer. According to KPMG, the number of deals fell by only about 17% — from 10,097 in Q4 2025 to 8,464 in Q1 2026. For a quarter with this level of capital concentration in five names, that is not a decline — it is a sign of resilience.

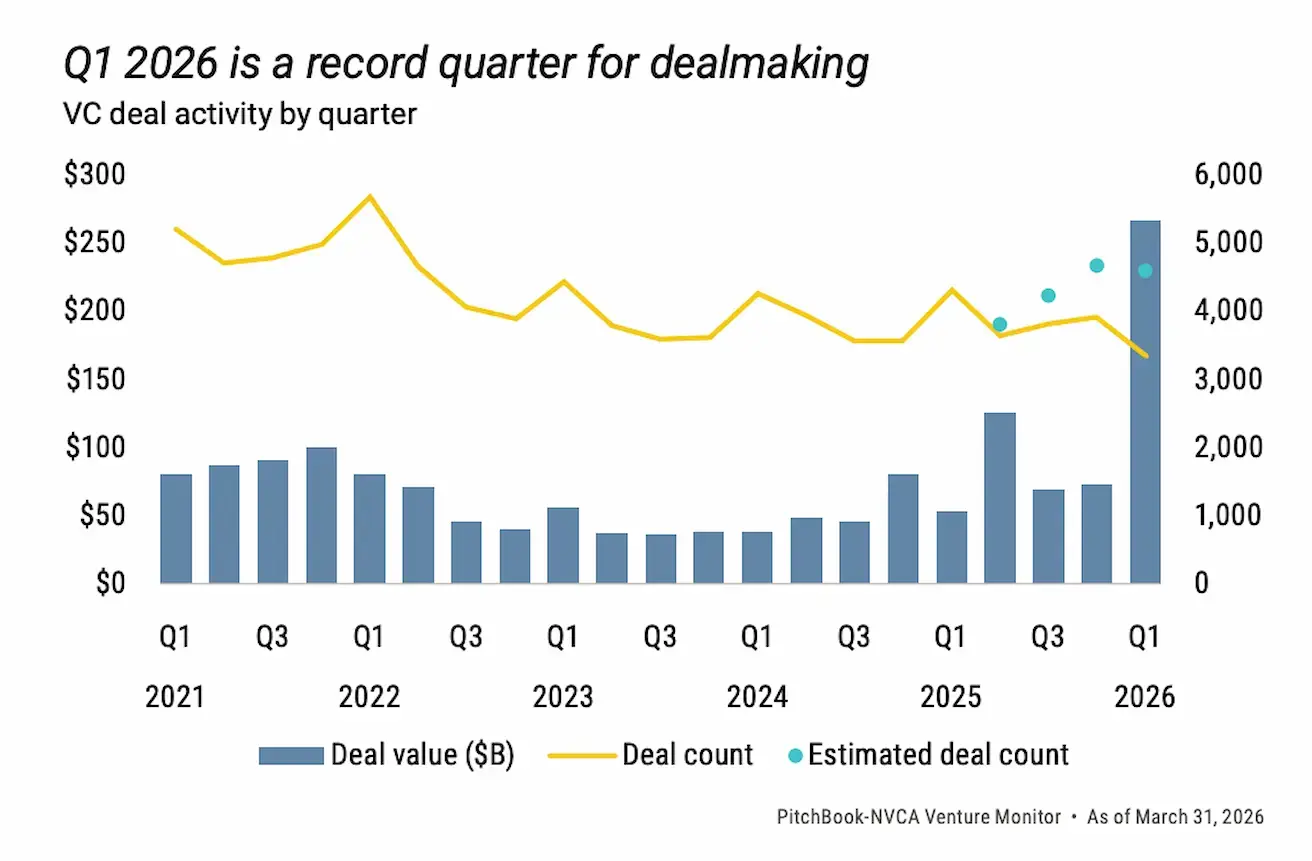

Chart: Investment volume and deal count by quarter over the past 5 years.

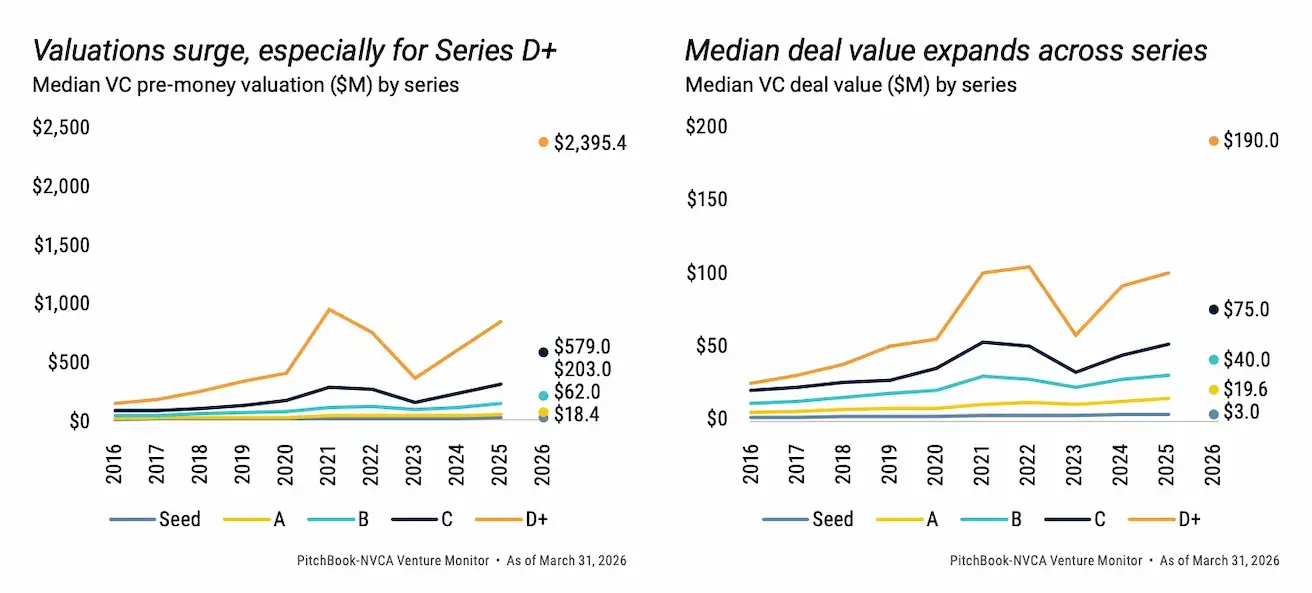

Broader market interest is further confirmed by valuation data. Median pre-money valuations are rising at every stage — from Seed to Series D+, where the median has reached $2.395 billion. Median deal size is also expanding across all stages.

Chart: Median pre-money valuation by stage (left) and median deal size by stage (right).

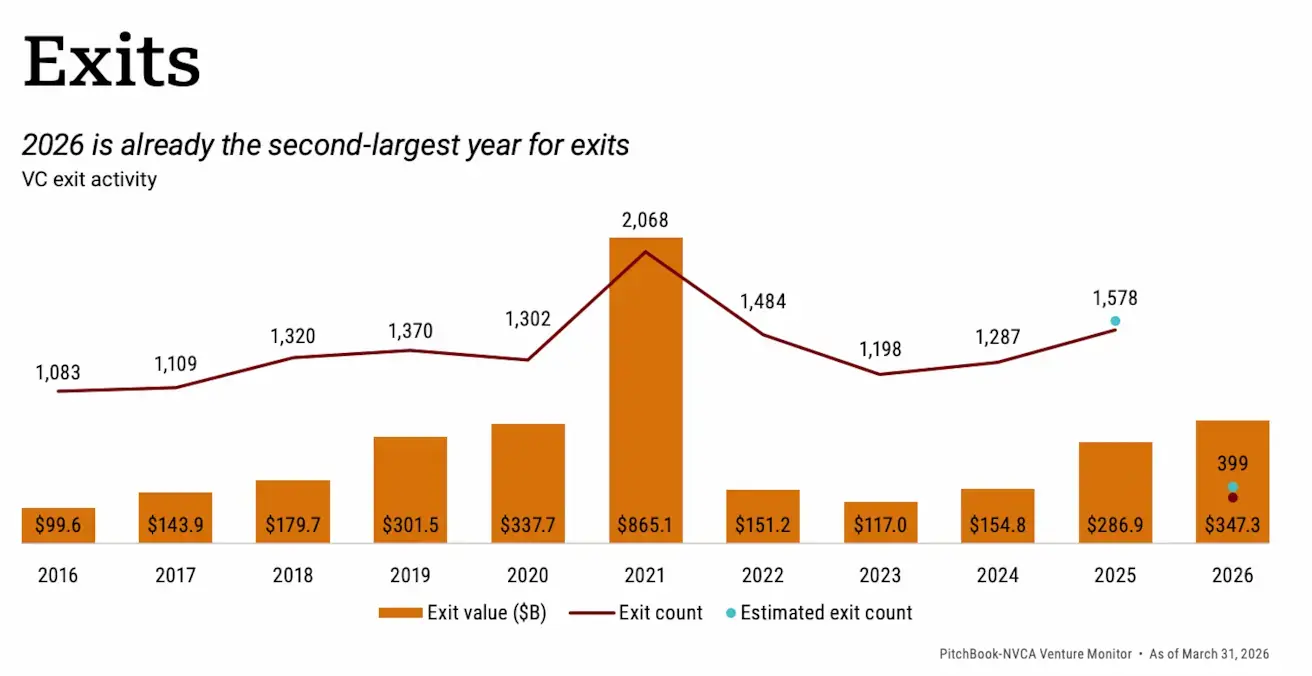

Exits: The Second-Largest Year on Record

Q1 set a record not only in investments but also in exit volume — $347.3 billion. On this measure, 2026 has already secured second place in venture exit history, trailing only 2021.

Chart: Exit deal volumes by year, 2016–2026.

Two deals drove the bulk of this result:

-

The merger of SpaceX and xAI: The transaction valued the combined company at $1.25 trillion, creating the most valuable private company in history. SpaceX acquired xAI for $250 billion in stock and cash.

-

Google's acquisition of Wiz for $32 billion. Beyond the price tag, the deal carries strategic weight: Google gained a strong AI team in cybersecurity and expanded the capabilities of its cloud services.

Together, xAI and Wiz generated $282 billion — accounting for 81.2% of the entire exit market for the quarter.

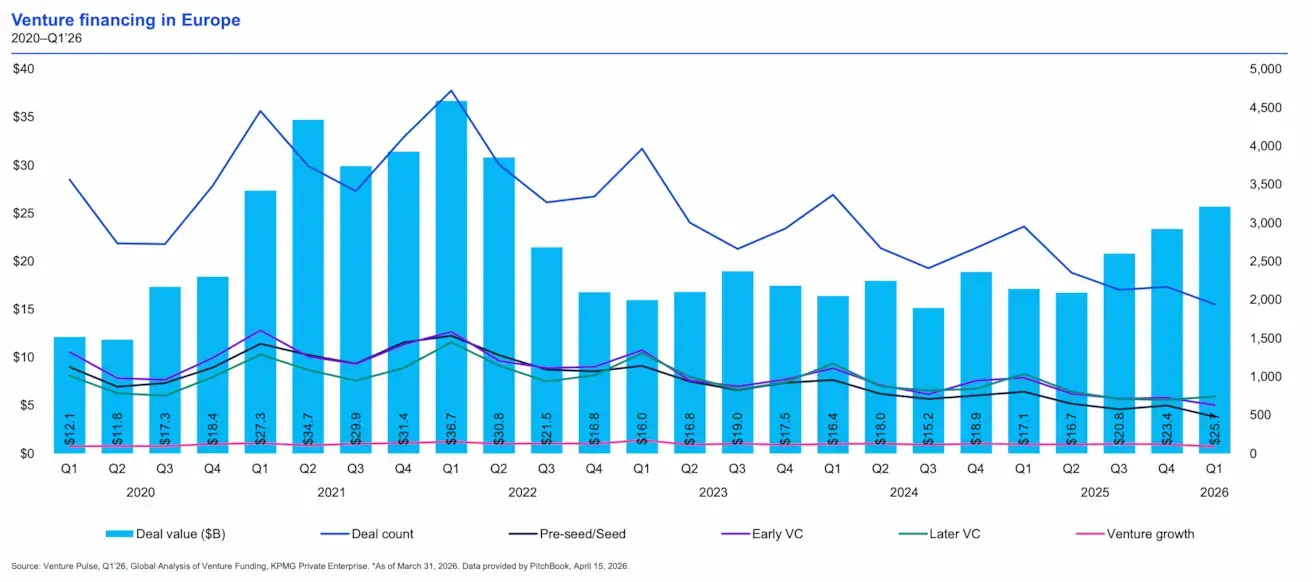

Europe and Asia: Growth Continues

While the US dominates the headlines, venture markets in Europe and Asia are gaining ground too. Europe has now posted three consecutive quarters of growth and is approaching the levels of the record period from Q1 2021 to Q2 2022. The key drivers are AI and the defense sector. In Q1 2026, European AI alone produced six megarounds, each exceeding $1 billion.

Chart: Investment volume and deal count by stage in European venture, 2020–2026.

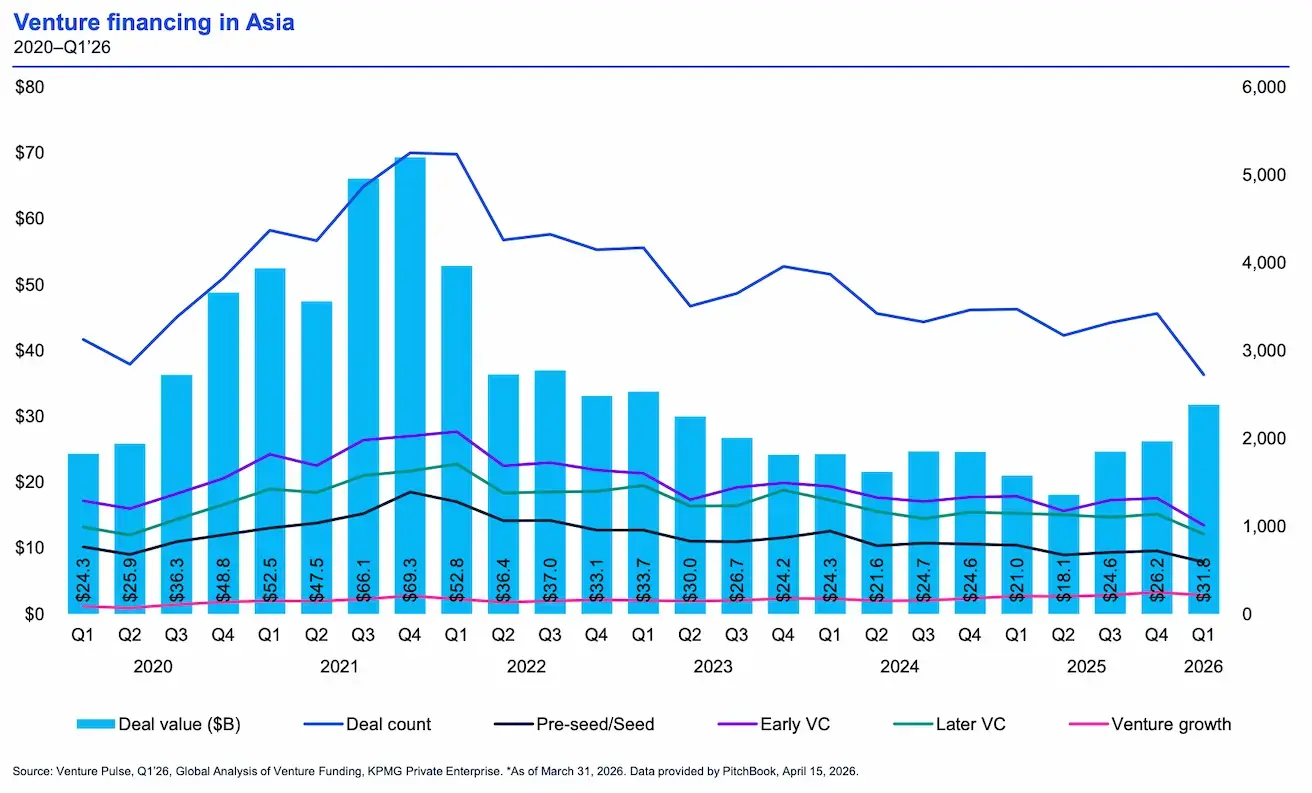

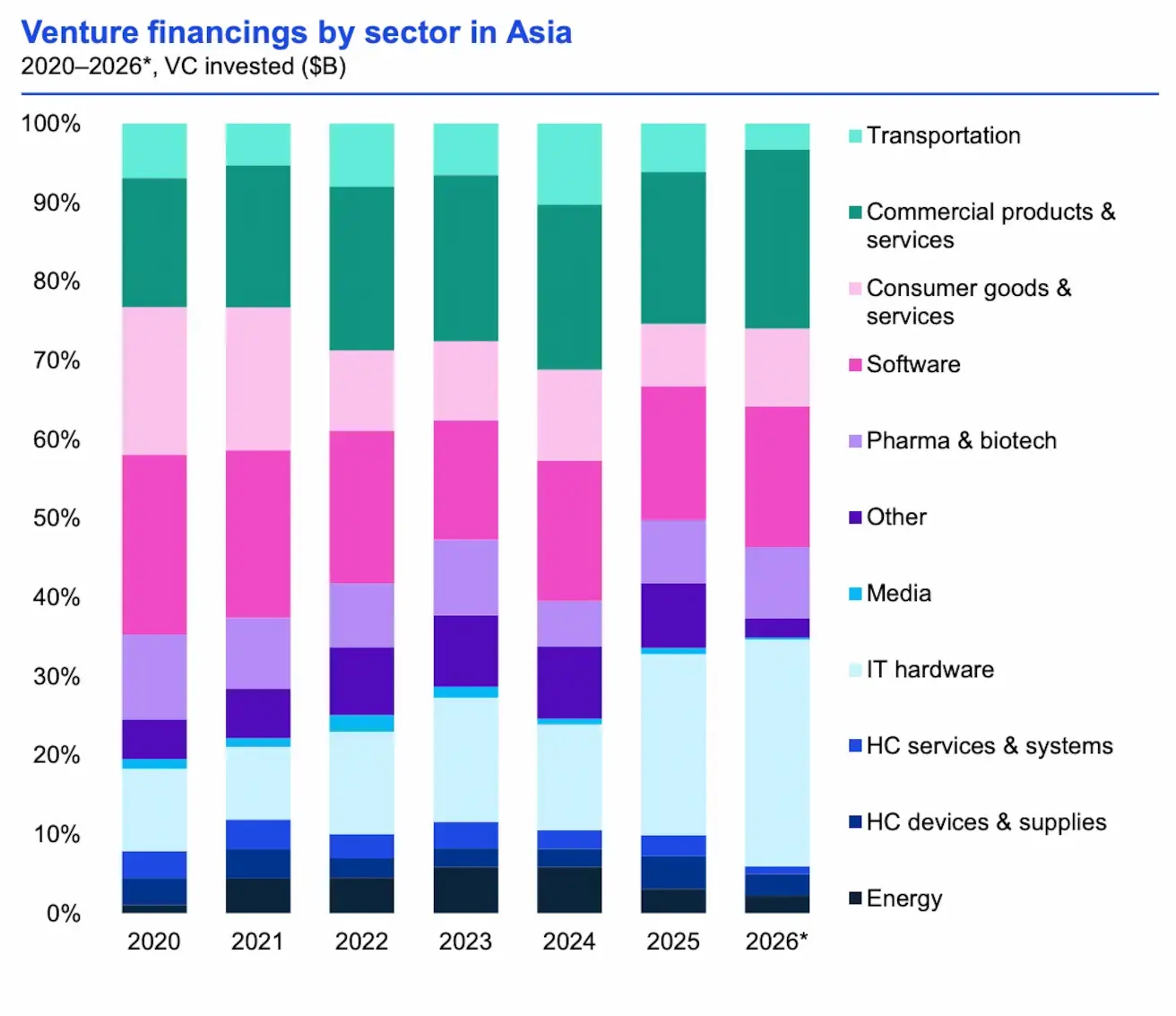

Asia is moving in the same direction — three quarters of consecutive growth, though the records of 2021–2022 remain out of reach for now. Electronics, AI, and biotech are leading the way. The exit market in the region pulled back from a strong Q4 2025, but remains above Q3 levels — a positive signal for a first quarter that has historically been quiet in Asia.

Chart: Investment volume and deal count by stage in Asian venture, 2020–2026.

It is worth highlighting a structural difference between the two largest markets:

-

In the US, the AI boom is financed by venture capital drawn from two main sources: funds raised during the 2021 vintage, and fresh capital flowing in on the back of strong corporate venture interest. This pool is large enough that the biggest companies feel no urgency to go public.

-

In China, the picture is different. Even with state support, AI companies face a funding gap in infrastructure, and as a result, they move toward IPOs much earlier. In Q1, two significant names went public: Zhipu AI (developers of the GLM model series) and MiniMax Group (multimodal models, including Hailuo AI, well known in China).

Chart: Asian venture capital distribution by sector.

Summary: Records With Nuance

Q1 2026 was a historically strong quarter — record investment and exit volumes, rising valuations at every stage, and sustained activity beyond the top five deals. Taken together, this shows that the market is not simply funneling capital into a handful of AI giants. It continues to function as a full ecosystem.

At the same time, capital remains concentrated: five rounds accounted for nearly three-quarters of total volume. That is not an anomaly, nor a cause for alarm — but it is a factor worth keeping in mind when reading the headline numbers.